Blockchain: Difference between revisions

| Line 467: | Line 467: | ||

There is no perfect monetary system for every situation. Bitcoin is not going to be the one world currency, and it doesn’t need to be. A lot of people compare Bitcoin to the Internet, but it’s more like CompuServe. It’s the first of many digital, non-state currencies to come, that will all interoperate with each other in ways we can’t even dream of yet." | There is no perfect monetary system for every situation. Bitcoin is not going to be the one world currency, and it doesn’t need to be. A lot of people compare Bitcoin to the Internet, but it’s more like CompuServe. It’s the first of many digital, non-state currencies to come, that will all interoperate with each other in ways we can’t even dream of yet." | ||

(http://falkvinge.net/2013/11/06/bitcoins-real-revolution-isnt-hard-money-its-economic-panarchy/ ) | (http://falkvinge.net/2013/11/06/bitcoins-real-revolution-isnt-hard-money-its-economic-panarchy/ ) | ||

==The key questions about the blockchain== | |||

Alanna Krause: | |||

1. Ethereum and similar blockchain enabled systems may distribute the verification of the ledger, but they are still centralised systems that easily become controlled by a few big players with more infrastructure resources. The contracts and transaction ledger may be decentralised, but the infrastructure isn't. | |||

2. Decentralisation in and of itself will not lead to P2P principles, or more social justice. In face, it has just as much power to great exacerbate social inequality. The most likely outcome of widespread adoption of block-chain enabled decentralised technologies is simply increased efficiency and wealth for big banks and governments. The discourse around the blockchain does not seem to acknowledge this. This WILL be co-opted (already is). | |||

3. I sense a deep lack of understanding of the social dynamics behind truly P2P ways of working and living in the blockchain community. People seem to want to "program" away what I consider the real challenges of confronting power dynamics, synthesising diversity, meeting different human needs, balancing collaboration and autonomy, building high-trust networks, collective ownership and commons management, etc. You cannot fix these things with technology - technology will just magnify the underlying dynamics. This is related to my observations of the lack of diversity in these communities. | |||

4. People get all excited about the blockchain, but most of the things they seem to want to do with it could be achieved just as easily with a normal database. It seems like the cases where you actually need an objectively verifiable distributed ledger in a zero-trust system are quite rare in practice. If people want to run self-organising corporations, why haven't they make a start with a normal database already? Surely they can implement a blockchain once it scales or they run into a real need. Seems to me people are just excited about some new and shiny tech concept, and not actually into solving the deeper challenges of self-organisation. I have seen a LOT of money changing hands and ideas thrown around, but no living case studies of blockchain enabled networks of people doing real productive work and creating livelihoods and societies." | |||

(via email, May 2016) | |||

Revision as of 23:42, 17 May 2016

= "a distributed cryptographic ledger shared amongst all nodes participating in the network, over which every successfully performed transaction is recorded". [1]

Contextual Citation

"Why trust Bitcoin, or more specifically, why trust the technology that makes Bitcoin possible? In short, because it assumes everybody’s a crook, yet it still gets them to follow the rules."

- Morgen E. Peck [2]

An important warning on the blockchain as a centralized infrastructure:

"The need to replicate the whole chain of blocks on our computer is an insurmountable barrier to entry if you’re searching for an alternative to IBM, Amazon or Google. The Twister chain is still small, but think about how, to date, the initial synchronization for Bitcoin requires storage space of more than 65GB for the complete download of the blockchain. For any of us, having to reserve 65GB on our personal computers has a large cost. But for IBM, or Google, or any of the Chinese Bitcoin miners, it’s nothing. And let’s not even talk about the astronomical differences between the processing capabilities of the great monsters of scale compared to ours. Because blockchain is consensual, after a certain point of centralization, the rules of the system depend on very few users. For example, the bitcoin “update” would be unviable if the two more Chinese mining organizations had refused to implement it. A network of nodes designed this way has a power structure with clear centralizers—the owners of infrastructure—that in the end presents a threat to the distributed future of the Internet. In summary, when we use Blockchain technologies, the barrier to entry has a relatively small knowledge component—compiling and installing software—but an insurmountable infrastructure barrier beyond certain scales."

- Manuel Ortega [3]

Definition

Via Aeze Soo:

"A block chain is a distributed data store that maintains a continuously growing list of data records that are hardened against tampering and revision, even by operators of the data store's nodes. The most widely known application of a block chain is the public ledger of transactions for cryptocurrencies, such as bitcoin. This record is enforced cryptographically and hosted on machines running the software."

Description

1. by Jacob Aron:

"The true innovation of Bitcoin's mysterious designer, Satoshi Nakamoto, is its underlying technology, the "block chain". That fundamental concept is being used to transform Bitcoin – and could even replace it altogether.

So what is the block chain? It is a ledger of transactions that keeps Bitcoin secure and allows all users to agree on exactly who owns how many bitcoins. Each new block requires a record of recent transactions along with a string of letters and numbers, known as a hash, which is based on the previous block and produced using a cryptographic algorithm.

Miners, people who run the peer-to-peer Bitcoin software, randomly generate hashes, competing to produce one with a value below a certain target difficulty and thus complete a new block and receive a reward, currently 25 bitcoins. This difficulty means faking a transaction is impossible unless you have more computing power than everyone else on the Bitcoin network combined. Confused? Don't worry, ordinary Bitcoin users needn't know the details of how the block chain works, just as people with a credit card don't bother learning banking network jargon. But those who do understand the power of the block chain are realising how Nakamoto's technology for mass agreement can be adapted. "You can replace that agreement with all sorts of different things and now you have a really powerful building block for any kind of distributed system," says Jeremy Clark of Concordia University in Montreal, Canada." (http://www.newscientist.com/article/mg22129553.700-bitcoin-how-its-core-technology-will-change-the-world.html)

2. Primavera De Filippi

"For many, bitcoin — the distributed, worldwide, decentralized crypto-currency — is all about money … or, as recent events have shown, about who invented it. Yet the actual innovation brought about by bitcoin is not the currency itself but the platform, which is commonly referred to as the “blockchain” — a distributed cryptographic ledger shared amongst all nodes participating in the network, over which every successfully performed transaction is recorded.

And the blockchain is not limited to monetary applications. Borrowing from the same ideas (though not using the actual peer-to-peer network bitcoin runs on), a variety of new applications have adapted the bitcoin protocol to fulfill different purposes: Namecoin for distributed domain name management; Bitmessage and Twister for asynchronous communication; and, more recently, Ethereum (released only a month ago). Like many other peer-to-peer (P2P) applications, these platforms all rely on decentralized architectures to build and maintain network applications that are operated by the community for the community. (I’ve written before here in WIRED Opinion about one example, mesh networks, which can provide an internet-native model for building community and governance).

Thus, while they enable a whole new set of possibilities, blockchain-based applications also present legal, technical, and social challenges similar to those raised by other P2P applications that came before them, such as BitTorrent, Tor, or Freenet."

The Blockchain as a universal ledger

Dominic Frisby:

"Today there is a new system of digital record-keeping. Its impact could be equally large. It is called the blockchain.

Imagine an enormous digital record. Anyone with internet access can look at the information within: it is open for all to see. Nobody is in charge of this record. It is not maintained by a person, a company or a government department, but by 8,000-9,000 computers at different locations around the world in a distributed network. Participation is quite voluntary. The computers’ owners choose to add their machines to the network because, in exchange for their computer’s services, they sometimes receive payment. You can add your computer to the network, if you so wish.

All the information in the record is permanent – it cannot be changed – and each of the computers keeps a copy of the record to ensure this. If you wanted to hack the system, you would have to hack every computer on the network – and this has so far proved impossible, despite many trying, including the US National Security Agency’s finest. The collective power of all these computers is greater than the world’s top 500 supercomputers combined.

New information is added to the record every few minutes, but it can be added only when all the computers signal their approval, which they do as soon as they have satisfactory proof that the information to be added is correct. Everybody knows how the system works, but nobody can change how it works. It is fully automated. Human decision-making or behaviour doesn’t enter into it.

If a company or a government department were in charge of the record, it would be vulnerable – if the company went bust or the government department shut down, for example. But with a distributed record there is no single point of vulnerability. It is decentralised. At times, some computers might go awry, but that doesn’t matter. The copies on all the other computers and their unanimous approval for new information to be added will mean the record itself is safe.

This is possibly the most significant and detailed record in all history, an open-source structure of permanent memory, which grows organically. It is known as the blockchain. It is the breakthrough tech behind the digital cash system, Bitcoin, but its impact will soon be far wider than just alternative money." (https://aeon.co/essays/how-blockchain-will-revolutionise-far-more-than-money)

How it works

Morgan Peck:

"the blockchain is nothing more than a long string of transactions, each of which refers to an earlier record in the chain. But Bitcoin users do not directly make the updates to the blockchain. In order to transfer coins to someone else, you have to create a request and broadcast it over the Bitcoin peer-to-peer network. After that, it’s in the hands of the miners. They scoop up the requests and do a few checks to make sure that the signature is correct and that there are enough bitcoins to make the transaction; then they bundle the new records into a block and add it to the end of the blockchain.

All miners work independently on their own version of the blockchain. When they finish a new block, they broadcast it to the rest of their peers, who check it, accept it, add it to the end of the chain, and pick up their work from this new starting point.

The arrangement will work only if the miners agree on what the most recent version of the blockchain should look like. In other words, they all have to agree on a consensus version of it. But given the fact that they’re all strangers, they really have no reason to trust one another’s work. What’s to stop a miner from fiddling with earlier entries on the blockchain and undoing payments?

The strategy that Satoshi Nakamoto (Bitcoin’s pseudonymous architect) devised for establishing consensus in his system is widely considered to be a breakthrough in distributed computing.

“There have been consensus algorithms running since the eighties, where you come to consensus, providing a log of events on multiple machines, with all the machines participating in that network,” says Paul Snow, the founder of Factom, a service that condenses data and transfers it onto the Bitcoin blockchain. However, he says, these systems were successful only when the participants shared a common allegiance.

Bitcoin replaces that allegiance with mathematical confidence. Given the cryptographic proof required to commit a transaction, we can already be confident that only people who own bitcoins can spend them. But a bitcoin miner can also be confident that the other miners are not changing entries on the blockchain, because in Bitcoin there is no going backward.

That’s because the process of adding a new block to the blockchain is very difficult. Anyone who participates is required to devote large quantities of computing power—and therefore, electricity—toward running the new data through a set of calculations called hash functions. Only once this work is completed can the block be appended to the chain in a way that satisfies other miners on the network.

“You’re building a giant wall,” explains Peter Kirby, the president of Factom. “And every time you want to agree to something, you put a thousand bricks on top of it. And you agree to something else and put another thousand bricks on top of it. And that makes it very, very, very difficult for someone to change a brick way down at the bottom of the wall.”

...

A Nakamoto blockchain, then, becomes more secure as more people participate in the network. But why would they? In the case of Bitcoin, it’s because they are paid to do it. Every time a block gets solved, a virgin transaction is created with a handful of newly minted bitcoins signed over to the first miner who completed the work.

In old security models, you tried to lock out all of the greedy, dishonest people. Bitcoin, on the other hand, welcomes everyone, fully expecting them to act in their own self-interest, and then it uses their greed to secure the network.

“This is, I think, the main contribution,” says Ittay Eyal, a computer scientist at Cornell who studies Bitcoin along with other decentralized networks. “Bitcoin causes an attacker to be better off by playing along than by attacking it. The incentive system leads a lot of people to contribute resources toward the welfare of the system.”" (http://spectrum.ieee.org/computing/networks/the-future-of-the-web-looks-a-lot-like-bitcoin)

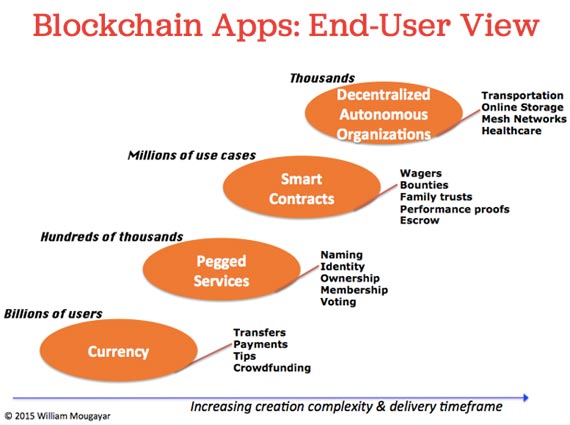

Typology

The four segments

Graphic at https://d3ansictanv2wj.cloudfront.net/blockchain_app-1c3df0ef526f707f181e2038a5f8fbab.jpg

{kind=link}

William Mougayar:

The Currency Segment

"The currency-related segment targets money transfers, payments, tips, or funding applications. The end-user typically goes to an exchange or uses their own wallet to conduct such transactions, benefiting from transaction cost reductions, speeds in settlements, and freedom from central intermediaries. Today’s exchanges are centralized, but it’s likely we’ll see another generation of decentralized trusted exchanges. And although the current bitcoin wallets today are “dumb” wallets, they could become smarter, via an ability to launch smart contracts.

The Pegged Services Segment

Pegged services to the blockchain represent an interesting segment because these apps utilize the blockchain’s atomic unit, which is a “value store” capability, but they also build on top of that with their unique off-chain services. For example, decentralized identity or decentralized ownership is a horizontal blockchain service, but it can be applied to any other vertical segments, such as for videos, music, or photography, just to name a few.

The Smart Contract segment

Smart contracts are small programs or scripts that run on a blockchain and govern legal or contractual terms on their own. They represent a simple form of decentralization. They will become available in a variety of application areas, such as for wagers, family trusts, escrow, time stamping, proofs of work delivery, etc. In essence, they are about moving certain assets or value from one owner to another, based on some condition or event, between people or things. Smart contracts represent an “intermediate state” between parties, and we will trust these smart programs to verify and take action based on the logic behind these state changes.

The DAO segment

Legal issues aside, a Distributed Autonomous Organization is “kind of” incorporated on the blockchain because its governance is very dependent on the end-users who are part-owners, part-users, and part-nodes on that decentralized network. Key aspects of a DAO are that each user is also a “worker,” and by virtue of their “work,” they contribute to the value appreciation of the DAO via their collective participation or activity levels. Arguably, bitcoin itself is the “uber DAO.” (https://www.oreilly.com/ideas/understanding-the-blockchain)

Technology

The Blockchain Application Stack

Joel Monegro:

"This is what I think the architecture of Internet applications is going to look like in 10 years. This is just a simple illustration and it leaves a lot of important insights and issues out. I’ll try my best to explain the thinking behind it below. To keep things short, we’ll run through every part of the stack from the bottom up, and do a deep dive on each in future posts.

The basic idea is that everything inside the gray rectangles is decentralized and open source. For now I’m calling these the shared data and protocol layers. Nobody controls these parts of the system, and they’re accessible by any person or company. If we use bitcoin as an example, the blockchain is the shared data layer and the bitcoin protocol is a decentralized protocol that’s part of the shared protocol Layer.

You’ll notice that each layer gets thinner the higher up you go. You’ll also notice that the shared data and protocol layers cover about 80% of the entire stack. Internet applications today are built on top of open, decentralized technologies like TCP/IP and HTTP, but if you were to graph the current Internet application stack like above, those open, decentralized protocols would probably only make up about 15% with everything on top being private and centralized.

1. Miners and the blockchain

If you know a little about how bitcoin works, you know what miners are. In a nutshell, miners are the nodes in a network of computers who, together, verify all bitcoin transactions. In exchange, the algorithm rewards them with bitcoin. Because bitcoin has real-world value, the operators of these machines are incentivized to keep them running. If you’d like to learn more about mining, this is a great explanation of how they work.

The blockchain is the public ledger that holds a permanent record of all bitcoin transactions, and is maintained by the miners. It’s not controlled by a single entity and it’s accessible by everyone. You can read more about the blockchain here.

2. Overlay networks

This is where things start to get interesting. Developers are starting to build networks that work in parallel to the bitcoin blockchain to perform tasks that the bitcoin network can’t, but that make use of the bitcoin blockchain to, for instance, timestamp or validate their work.

One example is Counterparty. Another might be sidechains. Whatever form these overlay networks take, the one thing they have in common is their connection to the bitcoin blockchain, and how they benefit from its network effects to achieve liquidity without having to bootstrap their own alternative cryptocurrency and/or blockchain like alternative solutions such as Ethereum require.

3. Decentralized protocols

Thanks to the blockchain, for the first time we can develop open source, decentralized protocols with built-in data (thanks to overlay networks and the blockchain), validation, and transactions that are not controlled by a single entity. This is where the traditional architecture of software businesses begins to break down. The best example of a decentralized protocol on top of a shared data layer is bitcoin, and we’re already well aware of how it’s affecting money and finance.

Companies like eBay, Facebook and Uber are very valuable because they benefit tremendously from the network effects that come from keeping all user information centralized in private silos and taking a cut of all the transactions.

Decentralized protocols on top of the blockchain have the potential to undo every single part of the stacks that make these services valuable to consumers and investors. They can do this by, for example, creating common, decentralized data sets to which any one can plug into, and enabling peer-to-peer transactions powered by bitcoin.

In fact, a number of promising teams have already begun working on the protocols that will disrupt the business models of the companies above. One example is Lazooz, a protocol for real-time ride sharing and another is OpenBazaar, a protocol for free, decentralized peer-to-peer marketplaces.

4. Open source and commercial APIs

Protocols are hard for the average developer to build on top of, so there’s an opportunity in making it easy to connect to them. Whether it’s a good business in the long term is up for debate, but I think it’s a very important part of the stack.

Making it quick and easy for developers of any skill set to quickly build an application and experiment on top of these decentralized protocols is paramount to their success.

These will be either commercial services or open source projects. Good examples of this trend are Chain's APIs and Coinbase’s Toshi for bitcoin. They both serve the same purpose, but Chain is a hosted, commercial service, and Toshi is open source.

5. Applications

This is the consumer-facing part of the stack. Applications built atop this architecture will, in most cases, work very similarly to the ones we have today – just like Coinbase works similarly to PayPal.

The big difference to consumers, however, is that because they are built on decentralized protocols, they will be able to talk to each other, just like different email applications and bitcoin wallets can interoperate.

One thing I like about this stack is that it’s growing from the bottom up. First we had miners, the blockchain, and bitcoin, and now we’re building everything else on top. As far as I know, the most significant revolutions in technology have been built this way." (http://www.coindesk.com/blockchain-application-stack/)

Business Models

Joel Dietz:

"There are currently a number of incentive structures surrounding blockchain technology and open source software:

(1) Contribute open source code and make money via services (i.e. Peter Todd’s consulting)

(2) Create a new close source software project based on the Bitcoin blockchain with a privately held speculative unit (i.e. legal equity in Coinbase)

(3) Create an new technology set plugged into the Bitcoin blockchain with a privately held speculative unit (i.e. legal equity in Blockstream/Sidechains)

(4) Create an entirely new unit with inherent utility on a new blockchain (BTC in Bitcoin, XRP in Ripple, ETH in Ethereum)

(5) Create an entirely new unit with inherent utility on the Bitcoin blockchain (MSC in Mastercoin, XCP in Counterparty)" (https://medium.com/@Swarm/the-second-wave-of-blockchain-innovation-270e6daff3f5)

Comparing the Incentive Models

Joel Dietz:

"For a long time, the primary model of open source software development has been in category one. The software itself is free. Hosting and other services around it are not. People can also build high value applications on top of the open source code, but these are usually closed source. This is the model that Ruby on Rails and other web frameworks have used fairly successfully as Joel Dietz has previously written.

The second model is the typical business model. In this, the structure of legal equity binds both investors and developers to a future value that may not be realized for several years. This typically creates a group of a few people who are highly committed to a particular outcome, but may naturally come into odds. Historically there is also no way to incentivize any of the parties beyond employees and investors that may also have a vested interest in the platform (i.e. power users).

The third model, by which I primarily refer to Sidechains, is still inchoate. In the Sidechains whitepaper it proposes demurrage as a method for incentivizing sidechain development. This seems to promote exactly the opposite set of incentives than what you would want. Effectively this means that assets on the main chain hold their value, while assets on a sidechain gradually decrease in value, while the difference is basically given away to miners. Also, the Sidechains project has no publicly stated business model, which is also a fairly significant concern. Any potential revenue on a service-based business will never be enough for the venture capitalists to get their necessary return, which basically forces them to either create a closed source product or otherwise leverage their position to “gate keep” and charge some sort of toll on network usage.

The fourth model, though strongly disliked by many, is ironically closest to Bitcoin itself. It states fundamentally that there can be a speculative unit with attached technological innovation that is acquired, and by which the speculators will benefit as both utility and network grows. The somewhat unique feature of Ethereum and a few other related projects (e.g. DarkCoin) is that unlike earlier “altcoins,” these new projects do have significant additional utility that is not found on the Bitcoin Blockchain.

Since all such projects extend the core Bitcoin technology with this additional utility, this effectively makes them competitors to the Bitcoin blockchain. Although early adopters and venture capitalist backers of Bitcoin had the hope that the network effects of Bitcoin would make it something like the TCP/IP protocal of internet money, it is entirely possible that some other competitor will surpass it. I suspect that whether or not this is the case will depend highly on whether or not anyone can make comparable utility and innovation compatible with Bitcoin.

This leads to a fifth model that was perhaps under-appreciated until Ethereum came along. This is the possibility that a metacoin, so called because it works via inserting metadata into Bitcoin transactions, could provide much of the increased utility provided via a smart contracting layer without creating its own blockchain.

Both four and five have very similar economic incentive structures. First of all, they are open to all participants and immediately liquid. Because of this it means that they naturally engage much more quickly a wider audience who are also incentivized to spread the word about that network. But, because of the immediate liquidity, there is no necessary long-term engagement. This affects both the development side and investing, and also means that there a fairly strong incentive to drive up the short time value for a project and exit at the peak. This likely results in a greater amount of capital, greater number of participants, with less depth. While potentially appropriate to the Facebook age, it is typically the case that startups require a few number of very intensely committed people due to the often intensely competitive nature of development, the occasional crisises that test resolve of key participants, and the general need for deferred compensation.

An additional problem is that none of these projects have evolved business models independent of the appreciation of their new asset class. All effectively depend on driving up the price by increasing the underlying utility of the unit and size of their related network, something that, while feasible, remains a questionable choice for anything that expects to be around in 5–10 years. Also, it is quite possible that price appreciation in such an asset is limited relative to the benefits traditionally associated with equity (i.e. 1000x returns on a successful software exit from an early investment). Since venture capital is generally structured as taking high rewards for high risk, projects with capped rewards impossible for them to undertake from an investment perspective.

Another very significant drawback is that even where economic incentives maybe aligned, there are basically no accountability structures due to the basically non-existant legal framework for entities receiving this sort of funding. In this case, Counterparty decided not to take funds whatsoever, whereas Ethereum structured their legal documentation to explicitly state that they were promising nothing in return whatsoever.

As Vitalik recently noted, Ethereum also has a problem of having a dual purpose “product” offering and an “investment” offering, something Swarm founder Joel Dietz called misaligned incentives in an early piece on economics of Ethereum. It is problems like these that have probably caused two out of three Counterparty founders to begin working for a private corporation (Overstock), presumably with some additional equity-based incentivization in addition to the base counterparty unit. In this case, the Counterparty ecosystem now has participants both in categories (4) and (2), with potential conflicts of interest between the participants in area (2), but also the possibility for larger ecosystem growth presuming that those conflicts can adequately be mediated.

So far we have only discussed the advantages and disadvantages of existing economic incentive structures. What about the future? What other possibilities can we expect to emerge?

The first “composite” offering has been proposed by Reddit. This is to take an existing equity offering and distribute the benefits downwards to community users via cryptocurrency. This is an incredible opportunity, because it illustrates one of the key benefits of this ‘open’ incentivization model, it actually directly compensates the community members who contribute to network growth.

The other model is Swarm itself, which, due to legal complexities, was deliberately vague about specific utility at the outset of its fundraising period, and instead described more generally the various categories of benefits that could be applied via these technologies (perk distribution, membership, privileged product access, financial rewards).

This was sometimes described as sort of crypto social-contract with the intention of providing as much value as possible to its users as the legal infrastructure was developed in order to do so. Much of this increased value depended on ability to structure agreements via smart contracts, which was a technology that did not even exist in any usable form until one week ago." (https://medium.com/@Swarm/the-second-wave-of-blockchain-innovation-270e6daff3f5)

Potential Applications

by Dominic Frisby:

"Coders are now developing ways to use blockchain tech for purposes beyond an alternative money system. From 2017, you will start to see some of the early applications creeping into your electronic lives.

One application is in decentralised messaging. Just as you can send cash to somebody else with no intermediary using Bitcoin, so can you send messages – without Gmail, iMessage, WhatsApp, or whoever the provider is, having access to what’s being said. The same goes for social media. What you say will be between you and your friends or followers. Twitter or Facebook will have no access to it. The implications for privacy are enormous, raising a range of issues in the ongoing government surveillance discussion.

We’ll see decentralised storage and cloud computing as well, considerably reducing the risk of storing data with a single provider. A company called Trustonic is working on a new blockchain-based mobile phone operating system to compete with Android and Mac OS.

Just as the blockchain records where a bitcoin is at any given moment, and thus who owns it, so can blockchain be used to record the ownership of any asset and then to trade ownership of that asset. This has huge implications for the way stocks, bonds and futures, indeed all financial assets, are registered and traded. Registrars, stock markets, investment banks – disruption lies ahead for all of them. Their monopolies are all under threat from blockchain technology.

Land and property ownership can also be recorded and traded on a blockchain. Honduras, where ownership disputes over beachfront property are commonplace, is already developing ways to record its land registries on a blockchain. In the UK, as much as 50 per cent of land is still unregistered, according to the investigative reporter Kevin Cahill’s book Who Owns Britain? (2001). The ownership of vehicles, tickets, diamonds, gold – just about anything – can be recorded and traded using blockchain technology – even the contents of your music and film libraries (though copyright law may inhibit that). Blockchain tokens will be as good as any deed of ownership – and will be significantly cheaper to provide.

The Peruvian economist Hernando de Soto Polar has won many prizes for his work on ownership. His central thesis is that lack of clear property title is what has held back so many in the Third World for so long. Who owns what needs to be clear, recognised and protected – otherwise there will be no investment and development will be limited. But if ownership is clear, people can trade, exchange and prosper. The blockchain will, its keenest advocates hope, go some way to addressing that.

Smart contracts could disrupt the legal profession and make it affordable to all, just as the internet has done with music and publishing

Once ownership is clear, then contract rights and property rights follow. This brings us to the next wave of development in blockchain tech: automated contracts, or to use the jargon, ‘smart contracts’, a term coined by the US programmer Nick Szabo. We are moving beyond ownership into contracts that simultaneously represent ownership of a property and the conditions that come with that ownership. It is all very well knowing that a bond, say, is owned by a certain person, but that bond may come with certain conditions – it might generate interest, it might need to be repaid by a certain time, it might incur penalties, if certain criteria are not met. These conditions could be encoded in a blockchain and all the corresponding actions automated.

Whether it is the initial agreement, the arbitration of a dispute or its execution, every stage of a contract has, historically, been evaluated and acted on by people. A smart contract automates the rules, checks the conditions and then acts on them, minimising human involvement – and thus cost. Even complicated business arrangements can be coded and packaged as a smart contract for a fraction of the cost of drafting, disputing or executing a traditional contract.

One of the criticisms of the current legal system is that only the very rich or those on legal aid can afford it: everyone else is excluded. Smart contracts have the potential to disrupt the legal profession and make it affordable to all, just as the internet has done with both music and publishing.

This all has enormous implications for the way we do business. It is possible that blockchain tech will do the work of bankers, lawyers, administrators and registrars to a much higher standard for a fraction of the price.

As well as ownership, blockchain tech can prove authenticity. From notarisation – the authentication of documents – to certification, the applications are multifold. It is of particular use to manufacturers, particularly of designer goods and top-end electrical goods, where the value is the brand. We will know that this is a genuine Louis Vuitton bag, because it was recorded on the blockchain at the time of its manufacture.

Blockchain tech will also have a role to play in the authentication of you. At the moment, we use a system of usernames and passwords to prove identity online. It is clunky and vulnerable to fraud. We won’t be using that for much longer. One company is even looking at a blockchain tech system to replace current car- and home-locking systems. Once inside your home, blockchain tech will find use in the internet of things, linking your home network to the cloud and the electrical devices around your home.

From identity, it is a small step to reputation. Think of the importance of a TripAdvisor or eBay rating, or a positive Amazon review. Online reputation has become essential to a seller’s business model and has brought about a wholesale improvement in standards. Thanks to TripAdvisor, what was an ordinary hotel will now treat you like a king or queen in order to ensure you give it five stars. The service you get from an Uber driver is likely to be much better than that of an ordinary cabbie, because he or she wants a good rating.

There will be no suspect recounts in Florida! The blockchain will also usher in the possibility of more direct democracy

The feedback system has been fundamental to the success of the online black market, too. Bad sellers get bad ratings. Good sellers get good ones. Buyers go to the sellers with good ratings. The black market is no longer the rip-off shop without recourse it once was. The feedback system has made the role of trading standards authorities, consumer protection groups and other business regulators redundant. They look clunky, slow and out of date.

Once your online reputation can be stored on the blockchain (ie not held by one company such as TripAdvisor, but decentralised) everyone will want a good one. The need to preserve and protect reputation will mean, simply, that people behave better. Sony is looking at ways to harness this whereby your education reputation is put on the blockchain – the grades you got at school, your university degree, your work experience, your qualifications, your resumé, the endorsements you receive from people you’ve done business with. LinkedIn is probably doing something similar. There is an obvious use for this in medical records too, but also in criminal records – not just for individuals, but for companies. If, say, a mining company has a bad reputation for polluting the environment, it might be less likely to win a commission for a project, or to get permission to build it.

We are also seeing the development of new voting apps. The implications of this are enormous. Elections and referenda are expensive undertakings – the campaigning, the staff, the counting of the ballot papers. But you will soon be able to vote from your mobile phone in a way that is 10 times more secure than the current US or UK systems, at a fraction of the cost and fraud-free. What’s more, you will be able to audit your vote to make sure it is counted, while preserving your anonymity. Not even a corrupt government will be able to manipulate such a system, once it is in place. There will be no suspect recounts in Florida! The blockchain will also usher in the possibility of more direct democracy: once the cost and possibility of fraud are eliminated, there are fewer excuses for not going back to the electorate on key issues." (https://aeon.co/essays/how-blockchain-will-revolutionise-far-more-than-money)

Identity

Morgan Peck:

"So what can you do with a Nakamoto blockchain? The most simple applications, the ones we are likely to see in the near future, will make use of them as basic storage systems that take advantage of the unique properties of the network.

People who are interested in transparency and access are looking at the blockchain as a possible place to organize government records and to include the public in the legislative process, by giving people a forum for publishing, debating, and voting on new proposals.

Because the blockchain gives each entry a rough time stamp, it can also be used as a decentralized notary. Imagine, for example, taking a picture of a dent in your rental car and loading it into a Bitcoin transaction. By looking at what block the transaction went into, you could later prove that the dent existed before you left the parking lot.

Because Bitcoin transactions are secured by strong cryptography, the blockchain can also replace our standard user name–and–password strategy for identity verification. In such a system, a Bitcoin address could be tagged with a user name, while the private key would stand in as a password. Anyone could then ask you to prove your identity by using your private key to solve the same cryptographic puzzle that you would normally solve when making a Bitcoin transaction." (http://spectrum.ieee.org/computing/networks/the-future-of-the-web-looks-a-lot-like-bitcoin)

Censorship

Morgan Peck:

"Nakamoto blockchains also solve the problem of censorship. Once inserted into the chain, metadata cannot be removed. Developers have used this crucial feature to build a new censorship-resistant version of Twitter (called Twister), and a decentralized domain-name registry (Namecoin).

“Everything that we own, everything that we do, is governed by these big piles of records,” says Factom’s Kirby. “A bank is just a big stack of records. An insurance company is just a big stack of records. An economy is basically just a big stack of records. And if you can take this concept of…a giant global accounting ledger and say, ‘Now we can organize all the records in the world this way,’ well, it turns out that’s really exciting.” (http://spectrum.ieee.org/computing/networks/the-future-of-the-web-looks-a-lot-like-bitcoin)

Finance as a Commons, using the Blockchain

Raymond Aitken:

"What seems important is that it represents a distributed but powerful computing power, and incorruptible database, which can be used as a ledger-transactional system, as well as a notary system for publicly recording rights, including monetary/economic rights. In the event of a bail-in, the majority of the world's population and their enterprises, will have every incentive to transfer their accounts to such a system (which has a very different paradigm than Bitcoin).

My questions are:

(1) can the block-chain technology be architechtured into a decentralised operating system and commons block-chain platform, to provide banking as a public service, both at the local and international scale?

(2) Can it be architectured as the framework of a new international monetary system, in accordance with the proposals of the French-Swiss economist, Michel Laloux (whose book I am translating into English), so that

(3) money needed for regeneration of the economic commons (the 4 factors of production mentioned in my last email), as well as for solidarity (welfare) purposes - without dependency on the centralised State?" (email, August 2015)

Trust

Gideon Greenspan:

"If multiple entities are writing to the database, there also needs to be some degree of mistrust between those entities. In other words, blockchains are a technology for databases with multiple non-trusting writers.

You might think that mistrust only arises between separate organizations, such as the banks trading in a marketplace or the companies involved in a supply chain. But it can also exist within a single large organization, for example between departments or the operations in different countries.

What do I specifically mean by mistrust? I mean that one user is not willing to let another modify database entries which it “owns”. Similarly, when it comes to reading the database’s contents, one user will not accept as gospel the “truth” as reported by another user, because each has different economic or political incentives.

So the problem, as defined so far, is enabling a database with multiple non-trusting writers. And there’s already a well-known solution to this problem: the trusted intermediary. That is, someone who all the writers trust, even if they don’t fully trust each other. Indeed, the world is filled with databases of this nature, such as the ledger of accounts in a bank. Your bank controls the database and ensures that every transaction is valid and authorized by the customer whose funds it moves. No matter how politely you ask, your bank will never let you modify their database directly.

Blockchains remove the need for trusted intermediaries by enabling databases with multiple non-trusting writers to be modified directly. No central gatekeeper is required to verify transactions and authenticate their source. Instead, the definition of a transaction is extended to include a proof of authorization and a proof of validity. Transactions can therefore be independently verified and processed by every node which maintains a copy of the database.

But the question you need to ask is: Do you want or need this disintermediation? Given your use case, is there anything wrong with having a central party who maintains an authoritative database and acts as the transaction gatekeeper? Good reasons to prefer a blockchain-based database over a trusted intermediary might include lower costs, faster transactions, automatic reconciliation, new regulation or a simple inability to find a suitable intermediary.

So blockchains make sense for databases that are shared by multiple writers who don’t entirely trust each other, and who modify that database directly. But that’s still not enough. Blockchains truly shine where there is some interaction between the transactions created by these writers.

What do I mean by interaction? In the fullest sense, this means that transactions created by different writers often depend on one other. For example, let’s say Alice sends some funds to Bob and then Bob sends some on to Charlie. In this case, Bob’s transaction is dependent on Alice’s one, and there’s no way to verify Bob’s transaction without checking Alice’s first. Because of this dependency, the transactions naturally belong together in a single shared database.

Taking this further, one nice feature of blockchains is that transactions can be created collaboratively by multiple writers, without either party exposing themselves to risk. This is what allows delivery versus payment settlement to be performed safely over a blockchain, without requiring a trusted intermediary.

A weaker case can also be made for situations where transactions from different writers are cross-correlated with each other, even if they remain independent. One example might be a shared identity database in which multiple entities validate different aspects of consumers’ identities. Although each such certification stands alone, the blockchain provides a useful way to bring everything together in a unified way.

If we have a database modified directly by multiple writers, and those writers don’t fully trust each other, then the database must contain embedded rules restricting the transactions performed.

These rules are fundamentally different from the constraints that appear in traditional databases, because they relate to the legitimacy of transformations rather than the state of the database at a particular point in time. Every transaction is checked against these rules by every node in the network, and those that fail are rejected and not relayed on.

Asset ledgers contain a simple example of this type of rule, to prevent transactions creating assets out of thin air. The rule states that the total quantity of each asset in the ledger must be the same before and after every transaction." (http://www.multichain.com/blog/2015/11/avoiding-pointless-blockchain-project/)

Examples

BY PRIMAVERA DE FILIPPI:

"the blockchain is not limited to monetary applications. Borrowing from the same ideas (though not using the actual peer-to-peer network bitcoin runs on), a variety of new applications have adapted the bitcoin protocol to fulfill different purposes: Namecoin for distributed domain name management; Bitmessage and Twister for asynchronous communication; and, more recently, Ethereum (released only a month ago). Like many other peer-to-peer (P2P) applications, these platforms all rely on decentralized architectures to build and maintain network applications that are operated by the community for the community." (http://www.wired.com/2014/03/decentralized-applications-built-bitcoin-great-except-whos-responsible-outcomes/)

Ethereum

"One of those tapping into its power is Vitalik Buterin, a 19-year-old developer from Toronto, Canada. Last week he launched Ethereum, a new platform that will not just allow for multiple cryptocurrencies, as they are known, but also promises to host a range of decentralised applications on a single block chain. Making systems decentralised is appealing because the authorities will find them hard to shut down.

Initially, Ethereum users will be able to exchange bitcoins for a new currency – ether. Then, ether will be mined just like Bitcoin. But acquiring another form of digital money is not the point. Ethereum is meant to work like an operating system for cryptocurrencies. Developers can create apps, such as social networks or file storage, that sit on Ethereum's network as part of an app store.

Ethereum allows for the creation of complex, yet decentralised, economic tools like financial derivatives, in which two parties can bet on the rise and fall of an asset, or crop insurance that pays out to a farmer according to a weather data feed. Creating decentralised versions of Dropbox or eBay should be possible too, claims Buterin.

Other developers are attempting to achieve the same results by overlaying new code on the existing Bitcoin block chain. One example is the concept of "coloured" coins: with bitcoins labelled to represent other assets such as gold, cars or even houses, you transfer ownership when you trade the labelled coin.

Buterin says Ethereum is much more flexible. "Bitcoin is great as a form of digital money, but its scripting language is too weak for any kind of serious advanced applications to be built on top." (http://www.newscientist.com/article/mg22129553.700-bitcoin-how-its-core-technology-will-change-the-world.html)

Decentralized Autonomous Corporations

"One of the more advanced concepts being touted for a next-generation Bitcoin is the idea of decentralised autonomous corporations (DAC) – companies with no directors. These would follow a pre-programmed business model and are managed entirely by the block chain. In this case the block chain acts as a way for the DAC to store financial accounts and record shareholder votes.

In a way, Bitcoin is actually the first DAC, says Daniel Larimer, a developer in Blacksburg, Virginia. People who own bitcoins are shareholders in the company, which offers financial services, earns revenue through transaction fees and pays a salary to its employees, the miners. But no one is in charge.

Larimer has started his own DAC, called BitSharesX, which he says can perform the actions of a bank, lending other currencies to customers, who can provide BitShares as collateral. Other potential business models for a DAC include election services and lotteries, all run automatically. "The key to a DAC is that it should not depend on any one person." (http://www.newscientist.com/article/mg22129553.700-bitcoin-how-its-core-technology-will-change-the-world.html)

Official Records

Morgan Peck:

"Last year, Manuel Araoz, an Argentinean programmer who now works for BitPay, one of the original Bitcoin payment providers, created a service that enables users to condense any document and embed it into a transaction on the blockchain. A lot of people are now getting excited about the possibility of using this kind of application to store official records. The two examples that come up most often at conferences are property titles and documents proving “prior art” in intellectual property cases. In the case of titles, you’re basically layering a new form of property onto a Bitcoin transaction. Once a deed to a house is associated with a particular value on the Bitcoin blockchain, it can be transferred from party to party without the need for a paper trail.

In the case of prior art, a document embedded in the blockchain would carry with it a rough time stamp (depending on the rate at which new blocks are being added to the chain), which inventors could later use in patent disputes to prove that they had the first claim to an idea. The same solution would extend to any situation where a human notary was necessary.

According to Gavin Andresen, one of the developers who works on the core Bitcoin protocol, these applications could be especially useful for underdeveloped nations where governments lack a good way of tracking and transmitting official documents."

“I think the places where it makes the most sense are the places where they don’t already have a functioning system, they don’t have some legacy way of accomplishing something that the blockchain can help them accomplish,” says Andresen. “The example of property records, deeds to houses. Here in the United States, in Europe, and in other developed world nations, we have this whole system that’s all about keeping track of who owns property and then taxing them. There are parts of the world where that just doesn’t exist yet.” (http://spectrum.ieee.org/computing/networks/the-future-of-the-web-looks-a-lot-like-bitcoin/four-cool-things-you-can-do-with-the-blockchain)

Voting

Morgan Peck:

"There are several groups (Agora, BitCongress, Swarm) that are looking for ways to use the Bitcoin blockchain to enable online voting. Most of the schemes would involve sending a tiny fraction of a specially tagged bitcoin (or a similar token) to every voter. The voter could then sign it over to anyone on a list of candidates. The candidate with the most bitcoins at the end of the vote would win. One of the benefits of a system like this is that voters could divide their votes among candidates. The results are also completely transparent and visible to anyone who has downloaded a copy of the blockchain. On one hand, this is good because you can conduct a public audit of the vote. On the other hand, it opens the door for vote selling.

The BitCongress application, which is still under development, goes further and seeks to carve out a space for all the steps in governance. The group wants to provide a forum for debate, a process for voting, and a place for representatives to publish legislative proposals, all on the Bitcoin blockchain." (http://spectrum.ieee.org/computing/networks/the-future-of-the-web-looks-a-lot-like-bitcoin/four-cool-things-you-can-do-with-the-blockchain)

Identity Verification

Morgan Peck:

"Today, when we need to log on to websites or applications, we usually prove our identities by supplying passwords. As a result, we are accustomed to managing many different passwords on many different websites. We are also trusting these Web services to keep our passwords, and therefore our identities, safe.

Onename uses the blockchain to link your name to a Bitcoin address, which you can then prove you control by signing a digital message with your private key (similar to what you do when you spend bitcoins). The developers describe the service as a universal passport for the Internet. They imagine that in the future, instead of signing in to applications with a Facebook account, we will refer to a Onename identity stored on the blockchain.

For example, “If you want to release your medical records to an application, it is important that you are in unique control of your medical records. You’re not going to trust Facebook,” says Ryan Shea, the cofounder of Onename. “This can even be extended to things like authorizing access to your home, opening your garage door, really any action that is tied to identity. So you could see this being used anywhere on the Web where identity is required.”

In this scenario, you never have to reveal your private key to anyone, and you retain complete control over (and responsibility for) the integrity of your online identity." (http://spectrum.ieee.org/computing/networks/the-future-of-the-web-looks-a-lot-like-bitcoin/four-cool-things-you-can-do-with-the-blockchain)

Distributed Domain-Name Server

Morgan Peck:

"Namecoin is an altcoin that was established in 2011. The code is nearly identical to that of Bitcoin, but it uses its own Nakamoto blockchain. Rather than tracking financial transactions, it records domain names and their corresponding IP addresses to provide a more secure, censorship-resistant alternative to the way we usually access websites on the Internet.

When you type a conventional URL (like Spectrum.ieee.org) into a browser, you rely on a centralized third party, called a domain-name server, to look up the URL in a directory and find the numerical IP address of the server you want to connect to. When the U.S. government wants to disable a website, one easy way is for it to demand that the domain-name server, or DNS, refuse to resolve the offending URL. In this case, even though the IP address you want is sitting there in a database on its server, the DNS sends you to a Digital Millennium Copyright Act website takedown notice instead of routing you to your destination. Because the databases are centralized, they are also good targets for hackers. If an attacker can manage to either change an IP address in the directory or send you a false one, he can divert your traffic toward a nefarious website.

Namecoin was created to solve both of these problems. With a Namecoin client, you can look up any .bit URL and be sure that the corresponding IP address is the same as the one that originally registered it.

“With Nakamoto blockchains, it’s very, very difficult to remove data from the blockchain once it’s already in there. And it’s not really feasible to insert fraudulent data that claims to be from an address that it really isn’t,” says Jeremy Rand, one of the Namecoin developers. “What this means is, if I register a name in the Namecoin blockchain, no one else can reverse that transaction and remove it from the blockchain, and no one else can hijack it.” (http://spectrum.ieee.org/computing/networks/the-future-of-the-web-looks-a-lot-like-bitcoin/four-cool-things-you-can-do-with-the-blockchain)

History

Joel Dietz:

" The Second Wave of Blockchain Innovation

The last months have included intense discussion on the feasibility and desirability of various economic forms of Blockchain innovation, including the ominous title of an article in Techcrunch, “A Bitcoin Battle is Brewing.” Although they contain many of the same principles that made Bitcoin successful, other digital assets have often been criticized and dismissed as “speculative.” However, recent usages of cryptoledger systems (c.f. “appcoins,” cryptoequity, smart contracts) often include substantial technological innovation and can be used to solve long standing problems both in investment and corporate governance.

History

In the mid-90s Nick Szabo, the inventor of smart contracts, noted the many fascinating things that could be done with programmable money. Another one of his best ideas, “Bit gold,” was later implemented as Bitcoin, a distributed network with unique incentivization mechanism for growth. It included a rudimentary scripting language that allowed you to send a unit, a “coin,” to another participant in the network. This was enough for it to rise in value from mere pennies to a high of over $1,000.

In 2013 J.R. Willet drafted “Second Bitcoin Whitepaper” and proposed that the Bitcoin blockchain be extended with more advanced smart contract capability, encoded via metadata. His proposed way to finance the development of this new functionality was to create a new type of token that gave access to these advanced features. This was called the “Master” coin.

J.R. sold $600,000 worth of Mastercoins for Bitcoins in the first ever “crowdsale” in the summer of 2013. By the end of that calendar year, they had appreciated 74x in value. Investors rejoiced. But not all was well in the world of Mastercoin. Instead of full-time developers crunching away in hope of some future event, founders weren’t working full time and most people were employed via “bounties.” All of the best developers interested in the idea were quietly drifting away from the project. These notably included Vitalik Buterin and Adam Krellenstein, both of whom would attempt to solve the same problem in their own way.

In early 2014, Adam Krellenstein, a self taught programmer, created a re-implementation of the Mastercoin idea from scratch. Like Mastercoin, it contained an implementation of certain smart contract ideas, primarily implementations of existing financial tools. This included asset issuance, asset trading, dividends, and betting. It was released as Counterparty and approximately $1.5mm worth of Bitcoin were transferred into this new system.

Around the same time, Vitalik Buterin developed the first proof of concept of Ethereum, an abstraction of the same idea. Instead of programming the specific desired features of smart contracts, Vitalik proposed creating a toolkit that allows anyone to program their own smart contract. While theoretically possible to implement in a similar context on the Bitcoin blockchain, Vitalik believed that there were many other aspects of Blockchain architecture that could be improved, including file storage, clearing times, and proofing against special hardware. Vitalik initiated his own crowdsale to finance this blockchain, which gathered approximately $15mm worth of Bitcoins.

As numerous other projects followed a similar model for funding in 2014, including Counterparty, Maidsafe, Storj, Supernet, Gems, and SWARM, there was a precipitous decline in the value of the progenitor. Mastercoins returned from a peak of almost 100 times return on investment to a price close to the original sale." (https://medium.com/@Swarm/the-second-wave-of-blockchain-innovation-270e6daff3f5)

Discussion

First, read this: The blockchain is a threat to the distributed future of the Internet!

Zacqary Adam Green:

"Bitcoin’s real contribution to the world is its source code. The blockchain, the network protocol, the cryptographic verification — anyone can take this and build a currency with any economic properties their community needs. I’m not convinced that bitcoin’s Austrian School properties can sustain a global (or even local) economy, but you know what? That’s okay. If I ever feel the bitcoin economy has become too unequal, unbalanced, or stagnant, it’s now trivial for me to start my own damn currency.

A single bitcoin belongs is a measurement like a centimeter, but the bitcoin community is a social network. People use bitcoin because other people they trade with use bitcoin. If my town is running low on bitcoin but has a lot of resources to share internally, we can create our own local currency to free up bitcoin for importing and exporting. Or I could join an online network of artists who work on one another’s projects, and we’d create our own internal currency that plays by whatever rules we need it to.

There is no perfect monetary system for every situation. Bitcoin is not going to be the one world currency, and it doesn’t need to be. A lot of people compare Bitcoin to the Internet, but it’s more like CompuServe. It’s the first of many digital, non-state currencies to come, that will all interoperate with each other in ways we can’t even dream of yet." (http://falkvinge.net/2013/11/06/bitcoins-real-revolution-isnt-hard-money-its-economic-panarchy/ )

The key questions about the blockchain

Alanna Krause:

1. Ethereum and similar blockchain enabled systems may distribute the verification of the ledger, but they are still centralised systems that easily become controlled by a few big players with more infrastructure resources. The contracts and transaction ledger may be decentralised, but the infrastructure isn't.

2. Decentralisation in and of itself will not lead to P2P principles, or more social justice. In face, it has just as much power to great exacerbate social inequality. The most likely outcome of widespread adoption of block-chain enabled decentralised technologies is simply increased efficiency and wealth for big banks and governments. The discourse around the blockchain does not seem to acknowledge this. This WILL be co-opted (already is).

3. I sense a deep lack of understanding of the social dynamics behind truly P2P ways of working and living in the blockchain community. People seem to want to "program" away what I consider the real challenges of confronting power dynamics, synthesising diversity, meeting different human needs, balancing collaboration and autonomy, building high-trust networks, collective ownership and commons management, etc. You cannot fix these things with technology - technology will just magnify the underlying dynamics. This is related to my observations of the lack of diversity in these communities.

4. People get all excited about the blockchain, but most of the things they seem to want to do with it could be achieved just as easily with a normal database. It seems like the cases where you actually need an objectively verifiable distributed ledger in a zero-trust system are quite rare in practice. If people want to run self-organising corporations, why haven't they make a start with a normal database already? Surely they can implement a blockchain once it scales or they run into a real need. Seems to me people are just excited about some new and shiny tech concept, and not actually into solving the deeper challenges of self-organisation. I have seen a LOT of money changing hands and ideas thrown around, but no living case studies of blockchain enabled networks of people doing real productive work and creating livelihoods and societies." (via email, May 2016)

The Blockchain's Major Design Flaw

- See: Blockchain - Discussion for more articles on the following topics:

Arthur Brock:

"Stop the Nonsensus! (Nonsense Consensus): Systems will never scale if you require global consensus for local actions by independent agents. For example, I should not have to know where every dollar in the economy is when I want to buy something from you. That adds an overhead of ridiculous complexity for something which needs to follow the principle of pushing intelligence and agency to the edges rather than center. Likewise, an atom should be able to bond with another atom (see cartoon) without accounting for status every electron in the universe. However, Bitcoin and blockchains are built around authorized tokens embedded in every transaction/record, which embeds unnecessary complexity and limitations for scalability into every interaction. Tokens are not what makes a decentralized system work, cryptographic signatures and self-validating data structures are.

Intrinsic Data Integrity: For a long time, data integrity has been conflated with the hosting, control, and access to the device on which the data is stored. So banks have big firewalls to keep you from hacking in and changing your account balance. But today we have self-validating data structures like hash-chains and Merkle-trees which leave evidence of tampering by breaking structural integrity, cryptographic hash, or counterparty signatures when the data is altered. This makes it possible to distribute the storage and management of data and ensure that the people holding it can't tamper with it. In other words, you could be an authority to show your own account balance, yet not be able to tamper with your account history. When implemented properly, this is the key to enabling massive scales of storage and throughput by enabling auditable data to be stored anywhere/everywhere instead of requiring agreement on single shared ledger.

Distributed Process not Consensus: Let's learn a bit from tracking how scalable systems in nature and real world get things done. Speakers of a language each carry the means to generate sentences as needed, we don't store every sentence spoken in some global ledger. Cells each carry a copy of their instruction set (DNA), rather than a record of the state and type of every cell. What you need to distribute in a system of collective intelligence is the ability to distribute reliable processing according to shared agreements. Consensus then becomes something used for to ensure the integrity of the processing, rather than the medium upon which processing is executed. This approach, lets you confirm that your copy of the process is valid, so you can rely on it to work according to the agreed upon rules and proceed authoritatively without having to wait for the rest of the network to validate, verify and update itself with your state.

Agents not Coins: Instead of starting with cryptographic coins or tokens as the fundamental thing that exists, start by having the agents/people/organizations (or their signatures and account IDs) be the primary things that exist. When each person has a copy of the process needed to participate, and their records are stored with intrinsic data integrity, that enable two people to perform a transaction without requiring approval or consensus of anyone else. My process audits your transaction chain to make sure you're in a valid state, yours audits my chain, and either rejects the transaction if it puts someone in an invalid state according to the coded agreements. I know, you have a lot of questions about to make sure this can happen reliably, but I'll drill into that later.

Fractal not Global: You would think that the existence of the web would have taught us already that we can have shared access to pretty reliable, referenceable, information without us all having identical copies of it. Starting by creating a global ledger where each copy has to be in the same state is a totally different problem than having a fractal process for creating and organizing data which can be referenced by anyone wherever that data lives. It can still provide globally accessible agreement about data, but that agreement is constructed from fractally assembled reliable parts instead of requiring each part to reach global (or 51%) agreement to commit each element of data. One of the beautiful outcomes from this is such a massive reduction in the processing and storage requirements that it becomes feasible to run a full node on a mobile phone instead of requiring specialized mining hardware." (http://artbrock.com/blog/perspectives-blockchains-and-cryptocurrencies)

More Discussion

See: Blockchain - Discussion for more articles on the following topics:

1 From the Invisible Hand to the Visible Hand

2 Disintermediating Banking and User Accounts

3 Why the Bitcoin ledger is potentially so important

4 The Revolution will not be based on a global receipt depository!

5 The Political Vision behind the ledger

6 The Bitcoin Protocol Is More ‘Cloud’ Than ‘P2P’

7 What Are the Challenges?

8 Towards an internet of (block)chains

9 How the blockchain works for trust

10 The dispute on the size of blocks

The Blockchain Applications Directory

Compiled by Aeze Soo:

La Zooz

- Social Ride sharing :

→ https://www.youtube.com/watch?v=0BttJsLLOHo

→ LaZooz.org

" La’Zooz: The Decentralized, Crypto-Alternative to Uber [4]

Backfeed

Backfeed develops foundational tools for Decentralized Collaborative Organizations, syncing the spontaneous actions of millions of people to promote an era of collaboration and decentralized value production.

IPFS

A Permanent Web - A peer-to-peer hypermedia protocol → http://ipfs.io

Decentraland

- Virtual world - Blockchain → http://decentraland.org

Ascribe

- Creative commons on blockchain → http://cc.ascribe.io

Proof of Existence

To certify documents

→ http://proofofexistence.com → http://github.com/maraoz/proofofexistence

Group Currency

uCoin

- UBI currency :

Bitnation

- world : Virtual nation - Blockchain → http://www.bitnation.world

→ http://cryptonewsday.com/bitnation-releases-proof-of-concept-for-decentralized-government-platform/

Basic Income Co

BasicIncome.co : Economy - A peer-to-peer secure network → http://indiegogo.com/projects/basicincome-co-a-peer-to-peer-safety-net-network–2 → http://mybitnation.tumblr.com/post/105873406725/bitnation-announces-basic-income-application

OkTurtles

Foundation supporting beneficial decentralization technologies → http://okturtles.com

Open Bazaar

Trade online directly to other users, using Bitcoin → http://openbazaar.org

Alexandria Decentralized Library

→ https://www.cryptocoinsnews.com/alexandria-uses-block-chain-preserve-worlds-knowledge/

Virtual Notary

Attestation service → http://virtual-notary.org

Blocknet

A blockchain agnostic decentralized platform as a service

Blockcypher

Blockchain services

First Blockchain Incorporated

(NOT) The World’s First Stateless Company Incorporated In And By The Bitcoin Blockchain → http://firstblockchain.com

Blockchain Me

A tool for creating verifiable IDs on the blockchain

→ Code source: https://github.com/kiaraRobles/blockchainMe

Finyear

Laboratory of ideas and innovations at Finyear (http://www.finyear.com/labs) → http://bl0ckcha1n.com

Factom

A scalable data layer for the blockchain → http://factom.org

Blockchain Summit

Summit blockchain → http://blockchainsummit.io

Eris Industries

The Distributed Application Platform → http://erisindustries.com

Bitmarkets

Voluntary : Bitmarkets → https://github.com/voluntarynet/Bitmarkets

Blockstream

Extending Bitcoin’s blockchain with Sidechains : → http://blockstream.com

Elements Project

Blockchain University

- Courses : → http://blockchainu.co

Blockchain London

Event - Conferences at London : → http://blockchainlondon.com

Institute for Blockchain Studies

→ http://blockchainstudies.org

Blockchain Info

Blockchain-Info : Explorator of Bitcoin blocks → http://blockchain.info

Bitcoin City

" Each city is a bitcoin transaction, on the road to the blockchain "

Crypto Graffiti

Store texts on the blockchain

Democracy OS

- "It’s time to design a system where we can delegate power to peers: people we can trust and hold accountable."

- "We’re beginning to see trust built on distributed networks. Will the blockchain change the way we build power ?"

- “We can secure power transactions (votes) making them valid in a network of peers where nobody is in charge.”

- "When you want to do online voting, the key element is identity validation."

- "We can build a democratic system where you don’t have to wait 3 years to change the people you delegated power to."

"Power on the blockchain - DemocracyOS" :

→ https://www.youtube.com/watch?v=YqOQS5wd6hU

Streamium IO

- Manuel Aráoz : “Going live at DecentralizeAll currently”

→ https://www.youtube.com/watch?v=8_tFSJTlKec

Blockchain Developer Assistance

"We help get developers on the blockchains" :

BlockStrap :

NeuroWare :

BlockchainSpace

More Information

- Read this first:

- Avoiding the pointless blockchain project

- The blockchain is a threat to the distributed future of the Internet

All about crypto-currencies → http://www.coinwarz.com/cryptocurrency/coins

Documentary : Ulterior States [ IamSatoshi Documentary ]→ https://www.youtube.com/watch?v=yQGQXy0RIIo

DecentralizeFM : → https://decentralize.fm

Book - Eyrolles - "Blockchain: Blueprint for a New Economy" → http://amazon.fr/Blockchain-Blueprint-Economy-Melanie-Swan-ebook/dp/B00SNS9JLW

http://www.economist.com/news/special-report/21650295-or-it-next-big-thing

The draw and blockchain ( in french ) → http://dem0crat1e.fr/posts/tirage-au-sort-bitcoin

Related entries: