Blockchain

= "a distributed cryptographic ledger shared amongst all nodes participating in the network, over which every successfully performed transaction is recorded". [1]

See, from Rachel O'Dwyer: How the Blockchain Might Support a Commons

For a word of caution, read this

Contextual Citation

"Why trust Bitcoin, or more specifically, why trust the technology that makes Bitcoin possible? In short, because it assumes everybody’s a crook, yet it still gets them to follow the rules."

- Morgen E. Peck [2]

An important warning on the blockchain as a centralized infrastructure:

"The need to replicate the whole chain of blocks on our computer is an insurmountable barrier to entry if you’re searching for an alternative to IBM, Amazon or Google. The Twister chain is still small, but think about how, to date, the initial synchronization for Bitcoin requires storage space of more than 65GB for the complete download of the blockchain. For any of us, having to reserve 65GB on our personal computers has a large cost. But for IBM, or Google, or any of the Chinese Bitcoin miners, it’s nothing. And let’s not even talk about the astronomical differences between the processing capabilities of the great monsters of scale compared to ours. Because blockchain is consensual, after a certain point of centralization, the rules of the system depend on very few users. For example, the bitcoin “update” would be unviable if the two more Chinese mining organizations had refused to implement it. A network of nodes designed this way has a power structure with clear centralizers—the owners of infrastructure—that in the end presents a threat to the distributed future of the Internet. In summary, when we use Blockchain technologies, the barrier to entry has a relatively small knowledge component—compiling and installing software—but an insurmountable infrastructure barrier beyond certain scales."

- Manuel Ortega [3]

Definition

0. From the Report on Blockchain Technology and Polycentric Governance:

"“Blockchain technology" represents a decentralized digital ledger of transactions. It securely records transactions across numerous computers, ensuring integrity and resistance to tampering, all without reliance on any central authority for its operation. "Blockchain systems" refer to the community of individuals and organizations involved in the development, management, and use of these blockchain networks and the applications built upon them."

([4]

1. Via Aeze Soo:

"A block chain is a distributed data store that maintains a continuously growing list of data records that are hardened against tampering and revision, even by operators of the data store's nodes. The most widely known application of a block chain is the public ledger of transactions for cryptocurrencies, such as bitcoin. This record is enforced cryptographically and hosted on machines running the software."

2. Via the Wikipedia:

"A block chain, or blockchain, is a distributed database that maintains a continuously-growing list of data records hardened against tampering and revision. It consists of data structure blocks—which hold exclusively data in initial blockchain implementations, and both data and programs in some (for example, Ethereum) of the more recent implementations—with each block holding batches of individual transactions and the results of any blockchain executables. Each block contains a timestamp and information linking it to a previous block.

The block chain is seen as the main technical innovation of bitcoin, where it serves as the public ledger of all bitcoin transactions. Bitcoin is peer-to-peer, every user is allowed to connect to the network, send new transactions to it, verify transactions, and create new blocks, which is why it is called permissionless. This original design has been the inspiration for other cryptocurrencies and distributed databases."

(https://en.m.wikipedia.org/wiki/Block_chain_(database))

3. Syed Omer Husain, Alex Franklin, et al. :

"Put simply, blockchain is a shared cryptographic register. It records transactions between two parties in a permanent and verifiable manner without the need for any intermediary or central authority. Though blockchains themselves can be seen as a development that drew from and combined many existing technologies (Campbell-Verduyn 2017), in this article, we situate them as the meeting point of two historical trajectories: the ledger and the Internet."

(https://link.springer.com/article/10.1007/s11625-020-00786-x)

4. Arna VB:

"What is Blockchain?

As the name suggests, blockchain, (consists) of:

- “Blocks” containing information which are “chained“ together through special mechanism of “cryptography“ forming a decentralised database in which data can’t be changed (immutable) once updated.

This information in blocks can vary in different blockchains:

- In case of Bitcoin: Record of Transactions

- In Case Of Ethereum: Code (Smart Contracts)."

Description

0. David Andolfatto:

"All record-keeping systems (which include monetary systems) must contend with trust issues and methods of organizing historical information. Conventional systems rely on the reputation of central authorities and record-keepers to achieve consensus. Blockchain, which powers Bitcoin, differs from conventional systems by achieving consensus through a community of anonymous (and therefore "trustless") agents who compete amongst themselves to authenticate transactions. The promise of the blockchain protocol is that it is invulnerable to human foibles." (https://research.stlouisfed.org/publications/review/2018/02/13/blockchain-what-it-is-what-it-does-and-why-you-probably-dont-need-one/)

1. by Jacob Aron:

"The true innovation of Bitcoin's mysterious designer, Satoshi Nakamoto, is its underlying technology, the "block chain". That fundamental concept is being used to transform Bitcoin – and could even replace it altogether.

So what is the block chain? It is a ledger of transactions that keeps Bitcoin secure and allows all users to agree on exactly who owns how many bitcoins. Each new block requires a record of recent transactions along with a string of letters and numbers, known as a hash, which is based on the previous block and produced using a cryptographic algorithm.

Miners, people who run the peer-to-peer Bitcoin software, randomly generate hashes, competing to produce one with a value below a certain target difficulty and thus complete a new block and receive a reward, currently 25 bitcoins. This difficulty means faking a transaction is impossible unless you have more computing power than everyone else on the Bitcoin network combined. Confused? Don't worry, ordinary Bitcoin users needn't know the details of how the block chain works, just as people with a credit card don't bother learning banking network jargon. But those who do understand the power of the block chain are realising how Nakamoto's technology for mass agreement can be adapted. "You can replace that agreement with all sorts of different things and now you have a really powerful building block for any kind of distributed system," says Jeremy Clark of Concordia University in Montreal, Canada." (http://www.newscientist.com/article/mg22129553.700-bitcoin-how-its-core-technology-will-change-the-world.html)

2. Primavera De Filippi

"For many, bitcoin — the distributed, worldwide, decentralized crypto-currency — is all about money … or, as recent events have shown, about who invented it. Yet the actual innovation brought about by bitcoin is not the currency itself but the platform, which is commonly referred to as the “blockchain” — a distributed cryptographic ledger shared amongst all nodes participating in the network, over which every successfully performed transaction is recorded.

And the blockchain is not limited to monetary applications. Borrowing from the same ideas (though not using the actual peer-to-peer network bitcoin runs on), a variety of new applications have adapted the bitcoin protocol to fulfill different purposes: Namecoin for distributed domain name management; Bitmessage and Twister for asynchronous communication; and, more recently, Ethereum (released only a month ago). Like many other peer-to-peer (P2P) applications, these platforms all rely on decentralized architectures to build and maintain network applications that are operated by the community for the community. (I’ve written before here in WIRED Opinion about one example, mesh networks, which can provide an internet-native model for building community and governance).

Thus, while they enable a whole new set of possibilities, blockchain-based applications also present legal, technical, and social challenges similar to those raised by other P2P applications that came before them, such as BitTorrent, Tor, or Freenet."

The Blockchain as a universal ledger

1. Dominic Frisby:

"Today there is a new system of digital record-keeping. Its impact could be equally large. It is called the blockchain.

Imagine an enormous digital record. Anyone with internet access can look at the information within: it is open for all to see. Nobody is in charge of this record. It is not maintained by a person, a company or a government department, but by 8,000-9,000 computers at different locations around the world in a distributed network. Participation is quite voluntary. The computers’ owners choose to add their machines to the network because, in exchange for their computer’s services, they sometimes receive payment. You can add your computer to the network, if you so wish.

All the information in the record is permanent – it cannot be changed – and each of the computers keeps a copy of the record to ensure this. If you wanted to hack the system, you would have to hack every computer on the network – and this has so far proved impossible, despite many trying, including the US National Security Agency’s finest. The collective power of all these computers is greater than the world’s top 500 supercomputers combined.

New information is added to the record every few minutes, but it can be added only when all the computers signal their approval, which they do as soon as they have satisfactory proof that the information to be added is correct. Everybody knows how the system works, but nobody can change how it works. It is fully automated. Human decision-making or behaviour doesn’t enter into it.

If a company or a government department were in charge of the record, it would be vulnerable – if the company went bust or the government department shut down, for example. But with a distributed record there is no single point of vulnerability. It is decentralised. At times, some computers might go awry, but that doesn’t matter. The copies on all the other computers and their unanimous approval for new information to be added will mean the record itself is safe.

This is possibly the most significant and detailed record in all history, an open-source structure of permanent memory, which grows organically. It is known as the blockchain. It is the breakthrough tech behind the digital cash system, Bitcoin, but its impact will soon be far wider than just alternative money." (https://aeon.co/essays/how-blockchain-will-revolutionise-far-more-than-money)

2. From the Report on Blockchain Technology and Polycentric Governance:

"In essence, a blockchain operates as a distributed digital ledger, spread out across numerous computers, designed to prevent any single party from gaining total control over the network. While the technology comes in various forms, “public and permissionless” blockchains stand out for using cryptographic methods to guarantee that the data on the ledger is transparent, open to all, and secure against unauthorized changes. These networks are built to be censorship-resistant, meaning no single authority can control or restrict access to the network or its transactions. Furthermore, blockchains have a global reach, with nodes of the network spread across the globe, making them not bound by national borders.

The origin of blockchain technology is attributed to an individual or group under the pseudonym of Satoshi Nakamoto, who in 2008 introduced the groundbreaking concept via the whitepaper “Bitcoin: A Peer-to-Peer Electronic Cash System” (Nakamoto 2008). Nakamoto's implementation of the first blockchain was designed to function as the public ledger for all transactions occurring on the Bitcoin network. This innovation marked the beginning of a new era in digital transactions. Since this initial invention, blockchain technology has undergone extensive evolution, extending its utility well beyond the confines of digital currencies. A significant milestone in this evolution was the introduction of the Ethereum network in 2014, which enhanced blockchain's functionality by introducing smart contracts. These are self-executing contracts with the terms of the agreement directly written into code, which activate automatically when predetermined conditions are met. The advent of smart contracts led to the development of decentralized applications (DApps) and decentralized autonomous organizations (DAOs), broadening blockchain's applicability. Currently, the versatility of blockchain is showcased through its myriad applications across diverse fields such as gaming, art, supply chain management, and identity verification, demonstrating its far-reaching impact.

Blockchain systems represent a sophisticated amalgamation of technology and social dynamics. They comprise the foundational blockchain technology and the network of individuals and organizations that develop, manage, and utilize it."

([5])

How it works

Morgan Peck:

"the blockchain is nothing more than a long string of transactions, each of which refers to an earlier record in the chain. But Bitcoin users do not directly make the updates to the blockchain. In order to transfer coins to someone else, you have to create a request and broadcast it over the Bitcoin peer-to-peer network. After that, it’s in the hands of the miners. They scoop up the requests and do a few checks to make sure that the signature is correct and that there are enough bitcoins to make the transaction; then they bundle the new records into a block and add it to the end of the blockchain.

All miners work independently on their own version of the blockchain. When they finish a new block, they broadcast it to the rest of their peers, who check it, accept it, add it to the end of the chain, and pick up their work from this new starting point.

The arrangement will work only if the miners agree on what the most recent version of the blockchain should look like. In other words, they all have to agree on a consensus version of it. But given the fact that they’re all strangers, they really have no reason to trust one another’s work. What’s to stop a miner from fiddling with earlier entries on the blockchain and undoing payments?

The strategy that Satoshi Nakamoto (Bitcoin’s pseudonymous architect) devised for establishing consensus in his system is widely considered to be a breakthrough in distributed computing.

“There have been consensus algorithms running since the eighties, where you come to consensus, providing a log of events on multiple machines, with all the machines participating in that network,” says Paul Snow, the founder of Factom, a service that condenses data and transfers it onto the Bitcoin blockchain. However, he says, these systems were successful only when the participants shared a common allegiance.

Bitcoin replaces that allegiance with mathematical confidence. Given the cryptographic proof required to commit a transaction, we can already be confident that only people who own bitcoins can spend them. But a bitcoin miner can also be confident that the other miners are not changing entries on the blockchain, because in Bitcoin there is no going backward.

That’s because the process of adding a new block to the blockchain is very difficult. Anyone who participates is required to devote large quantities of computing power—and therefore, electricity—toward running the new data through a set of calculations called hash functions. Only once this work is completed can the block be appended to the chain in a way that satisfies other miners on the network.

“You’re building a giant wall,” explains Peter Kirby, the president of Factom. “And every time you want to agree to something, you put a thousand bricks on top of it. And you agree to something else and put another thousand bricks on top of it. And that makes it very, very, very difficult for someone to change a brick way down at the bottom of the wall.”

...

A Nakamoto blockchain, then, becomes more secure as more people participate in the network. But why would they? In the case of Bitcoin, it’s because they are paid to do it. Every time a block gets solved, a virgin transaction is created with a handful of newly minted bitcoins signed over to the first miner who completed the work.

In old security models, you tried to lock out all of the greedy, dishonest people. Bitcoin, on the other hand, welcomes everyone, fully expecting them to act in their own self-interest, and then it uses their greed to secure the network.

“This is, I think, the main contribution,” says Ittay Eyal, a computer scientist at Cornell who studies Bitcoin along with other decentralized networks. “Bitcoin causes an attacker to be better off by playing along than by attacking it. The incentive system leads a lot of people to contribute resources toward the welfare of the system.”" (http://spectrum.ieee.org/computing/networks/the-future-of-the-web-looks-a-lot-like-bitcoin)

Characteristics

Seven tendencies of blockchain technology and the structural qualities that produce them

Sarah and Ben Manski:

- Verifiability

Transactions are assured through encrypted network consensus mechanisms in such a form that all transactions from the very first to the most recent are recorded in a ledger open to its maintainers, reducing information asymmetries2.

- Globality

Digital transactions and cultural information flows transcend geographic space and national borders3.

- Liquidity

Value liquidity is enhanced as the location of a store of value that does not depend or is not under the direct control of a sovereign, central bank or private corporation4.

- Permanence

The ledger of transaction is immutable by design5.

- Ethereality

Transactions are conducted in a digital medium6.

- Decentralization

The ledger is widely distributed among many stakeholders and maintainers.

- Future Focus

Found in newer developments of blockchain such as Ethereum, a stored autonomous self-reinforcing agency (SASRA) is formed in the temporal displacement of action through the use of smart contracts enabling the prefigurative recording of future transactions."

Game-based consensus mechanism

David Andolfatto:

"Fine, so you don't trust "the Man." What now? One alternative is to game the write privilege. The idea is to replace the trusted historian with a set of delegates drawn from the community (a set potentially consisting of the entire community). Next, have these delegates play a validation/consensus game designed in such a way that the equilibrium (say, Nash or some other solution concept) strategy profile chosen by each delegate at every date t = 1,2,3,... entails (i) no tampering with recorded history H(t-1) and (ii) only true blocks E(t) are validated and appended to the ledger H(t-1).

What we have done here is replace one type of faith with another. Instead of having faith in mechanisms that rely on personal reputations, we must now trust that the mechanism governing noncooperative play in the validation/consensus game will deliver a unique equilibrium outcome with the desired properties. I think this is in part what people mean when I hear them say "trust the math."

Well, trusting the math is one thing. Trusting in the outcome of a noncooperative game is quite another matter. The relevant field in economics is called mechanism design. I'm not going to get into details here, but suffice it to say that it's not so straightforward designing mechanisms with surefire beneficial properties. Ironically, mechanisms such as Bitcoin will have to build up trust the old-fashioned way—through positive user experience, much the same way most of us trust our vehicles to function, even if we have little idea how an internal combustion engine works.

Of course, the same holds true for games based on reputational mechanisms. The difference is, I think, that noncooperative consensus games are intrinsically more costly to operate than their reputational counterparts. The proof-of-work game played by Bitcoin miners, for example, is made intentionally costly (to prevent DDoS attacks) even though validating the relevant transaction information is virtually costless if left in the hands of a trusted validator. And if a lack of transparency is the problem for trusted systems, this conceptually separate issue can be dealt with by extending the read privilege communally.

Having said this, I think that, depending on the circumstances and the application, the cost associated with a game-based consensus mechanism may be worth incurring."

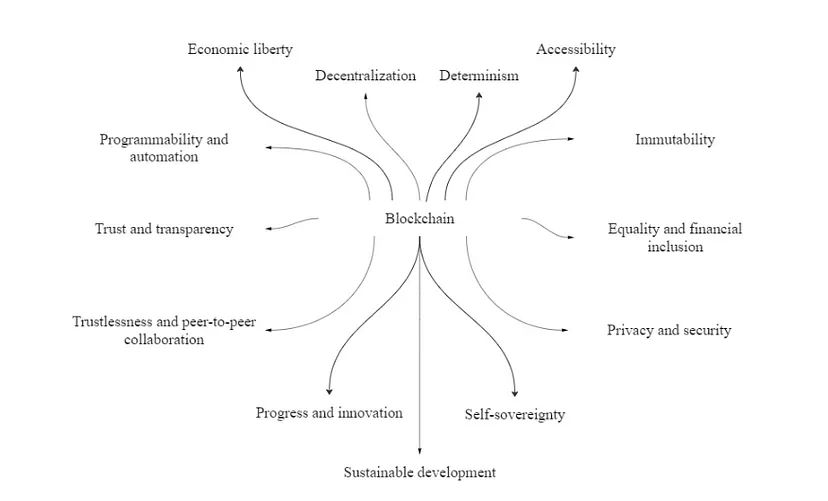

The thirteen philosophical pillars of the blockchain

Graph at https://miro.medium.com/v2/resize:fit:828/format:webp/1*HxQUzWm8dAZDsPKtVv9oCw.png

{kind=link}

1. Decentralization

Sasha Shilina:

Blockchain technology and cryptocurrencies are often associated with the principle of decentralization. This concept is rooted in political philosophy, particularly anarchist and libertarian ideas, that emphasize the need for decentralized power structures. Blockchain enthusiasts aim to create systems that distribute power, authority, and control across a network of participants rather than relying on centralized entities.

2. Trust and transparency

Blockchain technology offers a transparent and immutable ledger that records transactions and information. It aims to establish trust and remove the need for intermediaries or central authorities. This emphasis on transparency resonates with philosophical notions of truth, accountability, and open dialogue. It challenges traditional systems of trust and authority and encourages a more participatory and democratic approach.

3. Self-sovereignty

Blockchain technology emphasizes the concept of self-sovereignty, which means that individuals have control over their own data and identity. This is based on the idea of individual autonomy and the need for individuals to have agency over their own lives.

4. Privacy and security

Cryptocurrencies and blockchain systems incorporate cryptographic techniques to secure transactions and protect user privacy. They offer the possibility of pseudonymity and control over personal data, and some of them offer privacy. This aspect aligns with philosophical discussions around privacy rights, personal autonomy, and the limitations of surveillance capitalism. It encourages individuals to take ownership of their data and engage in self-determined interactions.

5. Programmability and automation

Automation is an important aspect of the philosophy behind blockchain. One of the key benefits of blockchain is that it allows for the automation of trust through the use of smart contracts, eliminating the need for intermediaries. Furthermore, blockchain technology also enables the automation of many other processes, such as record-keeping, identity verification, and supply chain management. This not only reduces the potential for human error and fraud but also increases efficiency and lowers costs. The idea of automation in the context of blockchain is rooted in the broader philosophy of automation, which seeks to replace manual labor and decision-making processes with machines and algorithms. Proponents of automation argue that it can increase productivity, reduce costs, and free humans from menial tasks to focus on more creative and innovative endeavors.

6. Immutability

Immutability refers to the idea that once data is recorded on a blockchain, it cannot be changed or deleted. This is because the ledger is distributed across the network, making it virtually impossible for any single user to alter the data without the consensus of the entire network. The rights given to the network’s participants are immutable and cannot be changed. In philosophy, the idea of unchanging, eternal truths has been explored by thinkers such as Plato, who posited the existence of a perfect, unchanging realm of Forms.

7. Trustlessness and peer-to-peer collaboration

Blockchain technology enables peer-to-peer interactions and disintermediation, allowing direct interactions and collaborations without intermediaries. This aspect resonates with philosophical ideas of horizontal relationships, cooperation, and the empowerment of individuals and communities. It challenges centralized power structures and promotes a more participatory and egalitarian approach to interactions and decision-making. The collaboration concept also resonates with the concept of consensus which can be traced back to the works of Ancient Greek philosophers and Enlightenment thinkers.

8. Equality and financial inclusion

Cryptocurrencies and blockchain-based financial systems have the potential to promote financial inclusion by providing access to financial services for individuals who are unbanked or underbanked. This aligns with philosophical concerns about justice, equality, and addressing socio-economic disparities. By offering financial agency and empowerment, blockchain and crypto can be seen as philosophies that strive for more inclusive and equitable systems.

9. Economic liberty

Economic liberty is a fundamental philosophical pillar of blockchain technology. It is rooted in the belief that individuals should have the freedom to conduct their economic activities without interference from governments or other centralized authorities. Blockchain enables economic liberty by providing a decentralized infrastructure that allows individuals to engage in peer-to-peer transactions without the need for intermediaries.

10. Accessibility

Accessibility is one of the key philosophical pillars of blockchain technology. It is the idea that the benefits of technology should be open to everyone, regardless of their socioeconomic status, education level, or technical expertise. Accessibility means that blockchain should be open and transparent, with no barriers to entry for individuals or organizations looking to participate. Also, at its core, accessibility in blockchain means that the technology should be designed in a way that makes it easy for anyone to use and participate in.

11. Sustainable development

Sustainable development is another philosophical pillar of blockchain. The decentralized and transparent nature of blockchain can contribute to the achievement of the United Nations Sustainable Development Goals (SDGs) aimed at ending poverty, protecting the planet, and ensuring peace and prosperity for all, creating a more equitable and sustainable world for future generations.

12. Progress and innovation

The pillar of progress and innovation refers to the continuous development and evolution of blockchain. This includes ongoing research and development, as well as the implementation of new features and functionalities that improve its capabilities and expand its potential use cases. It also involves fostering an environment that encourages innovation and experimentation, which is essential for the growth and adoption of innovative technologies.

13. Determinism

Determinism, one of the key philosophical pillars of blockchain, equals the finality concept. At its core, determinism is the idea that all events, including human actions, are ultimately determined by previous causes. This notion aligns with the idea of immutability in blockchain, where once a transaction is recorded on the ledger, it cannot be altered or deleted. In other words, the outcome of a transaction on the blockchain is predetermined and cannot be changed by any individual or entity. Determinism was developed by the Greek Pre-socratic philosophers, and later by Aristotle. Some of the main philosophers who have dealt with this issue are Thomas Hobbes, Baruch Spinoza, Gottfried Leibniz, David Hume, Arthur Schopenhauer, William James, Friedrich Nietzsche, Albert Einstein, Niels Bohr, and, more recently, John Searle, and Daniel Dennett."

Typology

""Swartz (2016) identifies two types of blockchain projects: radical and incorporative. Simply put, radical projects are oriented towards revolutionary social, economic, and political changes through imagining a new techno-political order. These systems enable users to circumvent the dominant institutional setting—central governments, banks, and corporations—by creating new ones. Contrastingly, incorporative projects innovate within the existing techno-political system not (necessarily) aiming for a reconstruction of the underlying political and social premises, but instead providing, for instance, more transparency and autonomy (Swartz 2016, pp. 86–87). As she clarifies, “the distinction…is not clearly defined and, in practice, there is a continuum between the two ideological modes” (Swartz 2016, p. 87). Often, we see how many radical start-ups which begin with “utopian visions might ‘pivot’ (to use industry parlance) towards business models different from or even in opposition to their original goals” (Swartz 2016, p. 88)." (https://link.springer.com/article/10.1007/s11625-020-00786-x)

See also: Typology of blockchain imaginaries, https://link.springer.com/article/10.1007/s11625-020-00786-x/tables/1

Private vs Public i.e. Permissioned vs Permissionless

RWA Report 2024:

Private Blockchains

▪ "The adoption of blockchain technology in general, regardless of private or public, could unlock significant efficiency gains for TradFi institutions with legacy infrastructure.

▪ Private blockchains enable privacy on two levels:

o Only permissioned participants can access the blockchain and transact / view its data

o The data is only stored by permissioned node operators

▪ It also simplifies the trust assumption, meaning consensus

mechanisms can be simplified further, e.g. Proof-of-Authority,

and could even go as far as enable certain participants to edit

past data.

▪ Simplifying consensus could also enhance the performance of the chain, providing higher throughput with little or no fees. ▪ Assuming these networks will operate with fewer nodes however, this will lead to heightened concentration of risk on the individual participants, node operators, and the maintainer of the blockchain client software.

▪ It is possible that a few participants or node operators going rogue or being exploited, or a bug in the client software, could cripple the network and cause irreparable damage to the chain and its data.

Public Blockchains

▪ In general, a key component of a public blockchain’s security is “strength in numbers”, where a large number of node operators secure the network. Broader dispersion of these operators across geographies and hardware, as well as use of different clients, make it difficult to launch 51% attacks against a public network.

▪ Another benefit of public blockchains is “building in the open”, where smart contract code is fully transparent. This could help get more eyes on smart contract codebases to ensure that they are free of vulnerabilities, and “battletested” in a real-world environment.

▪ However building on public blockchains also means sharing blockspace with the rest of the users, and the complications that come with that, such as occasional network congestion and resulting slower transaction times and higher gas fees.

▪ Transactions on a public blockchain are also publicly viewable by all (except specialized blockchains that enable privacy by default); A copy of the data for these chains are also stored by all node operators. These may not be preferable for certain use cases.

▪ Public blockchains are also not without its own technical hiccups, from occasional chain re-orgs to serious downtimes."

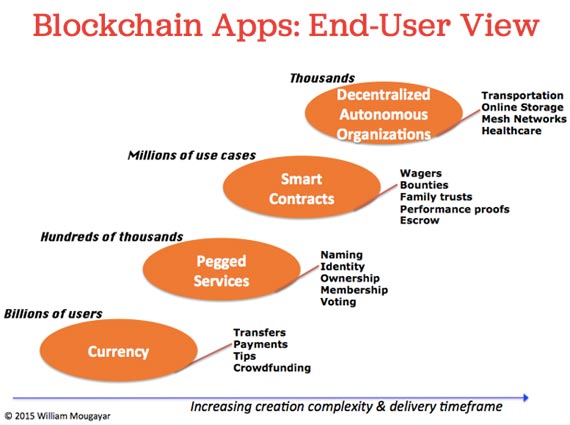

The four segments

Graphic at https://d3ansictanv2wj.cloudfront.net/blockchain_app-1c3df0ef526f707f181e2038a5f8fbab.jpg

{kind=link}

William Mougayar:

The Currency Segment

"The currency-related segment targets money transfers, payments, tips, or funding applications. The end-user typically goes to an exchange or uses their own wallet to conduct such transactions, benefiting from transaction cost reductions, speeds in settlements, and freedom from central intermediaries. Today’s exchanges are centralized, but it’s likely we’ll see another generation of decentralized trusted exchanges. And although the current bitcoin wallets today are “dumb” wallets, they could become smarter, via an ability to launch smart contracts.

The Pegged Services Segment

Pegged services to the blockchain represent an interesting segment because these apps utilize the blockchain’s atomic unit, which is a “value store” capability, but they also build on top of that with their unique off-chain services. For example, decentralized identity or decentralized ownership is a horizontal blockchain service, but it can be applied to any other vertical segments, such as for videos, music, or photography, just to name a few.

The Smart Contract segment

Smart contracts are small programs or scripts that run on a blockchain and govern legal or contractual terms on their own. They represent a simple form of decentralization. They will become available in a variety of application areas, such as for wagers, family trusts, escrow, time stamping, proofs of work delivery, etc. In essence, they are about moving certain assets or value from one owner to another, based on some condition or event, between people or things. Smart contracts represent an “intermediate state” between parties, and we will trust these smart programs to verify and take action based on the logic behind these state changes.

The DAO segment

Legal issues aside, a Distributed Autonomous Organization is “kind of” incorporated on the blockchain because its governance is very dependent on the end-users who are part-owners, part-users, and part-nodes on that decentralized network. Key aspects of a DAO are that each user is also a “worker,” and by virtue of their “work,” they contribute to the value appreciation of the DAO via their collective participation or activity levels. Arguably, bitcoin itself is the “uber DAO.”

(https://www.oreilly.com/ideas/understanding-the-blockchain)

Layers of the Blockchain Tech Stack

Blockchain Technology and Polycentric Governance:

The technological stack or “tech stack” refers to the combination of technologies used to construct and operate a specific project. In blockchain technology, this stack consists of various layers, each playing a unique role. These layers include blockchain networks, DApps, and DAOs, with blockchain networks further subdivided into layer 0, layer 1, and layer 2.

Layer 0 Blockchains: These provide the fundamental infrastructure for blockchain technology, serving as the bedrock upon which other layers are built. Layer 1 Blockchains: This layer consists of the blockchain protocol (which outlines the rules and procedures for data exchange, verification, and recording on the network) and the actual ledger that logs all transactions.

Layer 2 Blockchains: Aimed at enhancing the efficiency and speed of transactions, layer 2 blockchains act as scaling solutions for layer 1 blockchains, addressing issues like network congestion and high transaction fees.

DApps: These applications operate on a blockchain network rather than a centralized server or single computer. DApps represent a paradigm shift in application design and operation, utilizing blockchain's inherent security, transparency, and resilience benefits.

DAOs: DAOs are collaborative groups functioning via the Internet with a specific objective. They use smart contracts on blockchain networks and blockchain-based assets such as tokens and cryptocurrencies to manage governance processes.

Each layer of the tech stack can form distinct yet interconnected blockchain systems. The governance of the blockchain systems at the bottom affects the governance of the systems that are built on top. Naturally, members of blockchain systems at the top of the stack have incentives to participate in some governance decisions of blockchain systems at the bottom."

([6])

Governance Areas

Blockchain Technology and Polycentric Governance:

"The governance of blockchain systems is shaped not only by their placement within the technological stack but also by the specific nature and type of decisions that need to be made.

Across most blockchain systems, there are common decision-making areas that include:

Software Updates: These decisions involve updates or modifications to the software components that the blockchain relies on.

Monetary Policy: This area covers the issuance, distribution, and management of a cryptocurrency or token utilized by the blockchain system.

Treasury Allocation: Governance in this area concerns how to save, spend, or invest funds pooled together within the blockchain system.

Rewards to Contributors: This involves establishing policies and practices to acknowledge and reward the contributions made by community members.

Standards and Interoperability: These decisions focus on processes that enable the integration of the blockchain system with other platforms and projects within the broader blockchain ecosystem.

Security Measures and Breaches: This area usually involves exceptional governance processes or mechanisms, distinct from the standard governance areas, to address security-related issues.

Secondary Rules: These are meta-rules that govern how to create, amend, and repeal other governance rules within the system.

Additionally, for systems built around blockchain networks, a critical governance area is:

Block Production: This involves decisions on how new blocks of transactions are added to the ledger, guided by a predefined consensus algorithm. Each of these governance areas plays a crucial role in the effective functioning of blockchain systems, influencing everything from daily operations to long-term strategic direction. Understanding these areas is essential for comprehending the complex governance landscape of blockchain technology."

([7])

Stakeholders

Blockchain Technology and Polycentric Governance:

"In the governance of blockchain systems, various stakeholder groups play pivotal roles, engaging directly or indirectly in one or more governance areas.

These groups encompass a diverse range of participants, including:

Founders and Founding Teams: Individuals or groups who initiate and develop the blockchain project.

Software Developers: Professionals responsible for building and maintaining blockchain technology and its applications.

Organizations from the Broader Ecosystem: Entities that are either integrated with or competed with the referenced blockchain system. These might be other blockchain projects or businesses leveraging blockchain technology.

Investors: Individuals or entities that provide capital for the development and expansion of the blockchain system.

Token Holders: People who own cryptocurrencies or tokens associated with the blockchain, often having voting rights or other forms of influence in the system.

Users: End-users who interact with the blockchain system, either through transactions, applications, or other forms of engagement.

Policy Makers, Lawmakers, and Regulators: Governmental and regulatory bodies that influence the legal and operational framework within which blockchain systems operate.

It is important to note that overlap often exists within these stakeholder groups. For instance, core software developers may also be investors in the blockchain project. Each group behaves according to their own financial and non-financial incentives, which can sometimes lead to challenges in coordination and alignment of interests. Recognizing and understanding the diverse motivations and potential conflicts among these stakeholders is crucial for effective governance in blockchain systems."

([8])

Governance Mechanisms

Blockchain Technology and Polycentric Governance:

"Blockchain systems employ a variety of governance mechanisms to regulate themselves. These mechanisms can be split into on-chain and off-chain. On-chain Governance Mechanisms: Also referred to as “governance by the infrastructure,” these mechanisms are embedded directly within the blockchain's code, making them transparent and relatively resistant to change.

Key examples include:

Ex-ante rules and processes: Consensus algorithms used for block production in blockchain networks.

Ex-post rules and processes: On-chain signaling and voting systems designed for amending existing governance rules.

Off-chain Governance Mechanisms: Also known as “governance of the infrastructure,” these mechanisms involve decision-making processes that are not directly recorded on the blockchain.

This approach offers more flexibility but often lacks the transparency of on-chain mechanisms.

They include:

Community-driven mechanisms: In-person meetings, online forums, and off-chain voting, where the blockchain community collaborates and makes decisions in a more traditional, less technologically tethered manner.

External party-driven mechanisms: Laws, regulations from governmental agencies, and technology standards set by non-blockchain tech firms. These mechanisms influence blockchain governance from outside the blockchain community.

As noted by De Filippi and McMullen (2018), the choice between on-chain and off-chain governance mechanisms depends on the specific needs and context of the blockchain system, balancing transparency, flexibility, and responsiveness to internal and external influences."

([9])

Status

Igor Calzada, 2023:

(in the context of an article on E-Diasporas)

"After conducting the literature review and presenting empirical findings of cases and functionalities (Table 1), the positive contributions of blockchain can be summarized as follows:

1. Financial inclusion: Blockchain-based solutions such as cryptocurrencies and digital wallets, can promote greater financial inclusion by enabling low-cost, cross-border payments and remittances (Chouliaraki and Georgiou, 2022, Flore, 2018, Naik and Jenkins, 2020, Zhang and Morris, 2023).

2. Transparent and secure transactions: Blockchain’s distributed ledger technology provides a transparent and secure method for conducting transactions, fostering trust within e-diaspora communities (Werbach, 2019).

3. Decentralization: The decentralized nature of blockchain empowers e-diaspora communities to build peer-to-peer networks and circumvent traditional intermediaries, creating opportunities for collaboration and innovation (Inwood and Zappavigna, 2021, Zook, 2023).

4. Identity verification: Blockchain-based solutions can assist e-diaspora communities in establishing and verifying digital identities, protecting data privacy through the use of wallets (Calzada, 2023a). This is particularly valuable for individuals residing in regions with weak or unstable identity systems (Kondova & Erbguth, 2020).

However, there are also negative contributions to consider:

1. Energy consumption: The energy-intensive nature of blockchain can have adverse environmental effects, particularly in areas with limited access to renewable energy sources (Calzada, 2023c, Bridle, 2018).

2. Regulatory challenges: The decentralized nature of blockchain poses difficulties for regulation, giving rise to legal and regulatory challenges for e-diaspora communities (European Commission, 2020, Finck, 2018, UNESCO, 2023).

3. Lack of scalability: Current limitations in blockchain technology regarding scalability and speed may restrict its utility in certain contexts, especially when large-scale transactions or high-speed data processing are necessary (Hughes et al., 2019, Viano et al., 2023).

4. Security risks: While blockchain is generally considered secure, it is not impervious to security risks such as hacking and cyber-attacks, which can have negative repercussions for e-diaspora communities."

(https://www.sciencedirect.com/science/article/pii/S0016328723001623)

Technology

The Blockchain Application Stack

Joel Monegro:

"This is what I think the architecture of Internet applications is going to look like in 10 years. This is just a simple illustration and it leaves a lot of important insights and issues out. I’ll try my best to explain the thinking behind it below. To keep things short, we’ll run through every part of the stack from the bottom up, and do a deep dive on each in future posts.

The basic idea is that everything inside the gray rectangles is decentralized and open source. For now I’m calling these the shared data and protocol layers. Nobody controls these parts of the system, and they’re accessible by any person or company. If we use bitcoin as an example, the blockchain is the shared data layer and the bitcoin protocol is a decentralized protocol that’s part of the shared protocol Layer.

You’ll notice that each layer gets thinner the higher up you go. You’ll also notice that the shared data and protocol layers cover about 80% of the entire stack. Internet applications today are built on top of open, decentralized technologies like TCP/IP and HTTP, but if you were to graph the current Internet application stack like above, those open, decentralized protocols would probably only make up about 15% with everything on top being private and centralized.

1. Miners and the blockchain

If you know a little about how bitcoin works, you know what miners are. In a nutshell, miners are the nodes in a network of computers who, together, verify all bitcoin transactions. In exchange, the algorithm rewards them with bitcoin. Because bitcoin has real-world value, the operators of these machines are incentivized to keep them running. If you’d like to learn more about mining, this is a great explanation of how they work.

The blockchain is the public ledger that holds a permanent record of all bitcoin transactions, and is maintained by the miners. It’s not controlled by a single entity and it’s accessible by everyone. You can read more about the blockchain here.

2. Overlay networks

This is where things start to get interesting. Developers are starting to build networks that work in parallel to the bitcoin blockchain to perform tasks that the bitcoin network can’t, but that make use of the bitcoin blockchain to, for instance, timestamp or validate their work.

One example is Counterparty. Another might be sidechains. Whatever form these overlay networks take, the one thing they have in common is their connection to the bitcoin blockchain, and how they benefit from its network effects to achieve liquidity without having to bootstrap their own alternative cryptocurrency and/or blockchain like alternative solutions such as Ethereum require.

3. Decentralized protocols

Thanks to the blockchain, for the first time we can develop open source, decentralized protocols with built-in data (thanks to overlay networks and the blockchain), validation, and transactions that are not controlled by a single entity. This is where the traditional architecture of software businesses begins to break down. The best example of a decentralized protocol on top of a shared data layer is bitcoin, and we’re already well aware of how it’s affecting money and finance.

Companies like eBay, Facebook and Uber are very valuable because they benefit tremendously from the network effects that come from keeping all user information centralized in private silos and taking a cut of all the transactions.

Decentralized protocols on top of the blockchain have the potential to undo every single part of the stacks that make these services valuable to consumers and investors. They can do this by, for example, creating common, decentralized data sets to which any one can plug into, and enabling peer-to-peer transactions powered by bitcoin.

In fact, a number of promising teams have already begun working on the protocols that will disrupt the business models of the companies above. One example is Lazooz, a protocol for real-time ride sharing and another is OpenBazaar, a protocol for free, decentralized peer-to-peer marketplaces.

4. Open source and commercial APIs

Protocols are hard for the average developer to build on top of, so there’s an opportunity in making it easy to connect to them. Whether it’s a good business in the long term is up for debate, but I think it’s a very important part of the stack.

Making it quick and easy for developers of any skill set to quickly build an application and experiment on top of these decentralized protocols is paramount to their success.

These will be either commercial services or open source projects. Good examples of this trend are Chain's APIs and Coinbase’s Toshi for bitcoin. They both serve the same purpose, but Chain is a hosted, commercial service, and Toshi is open source.

5. Applications

This is the consumer-facing part of the stack. Applications built atop this architecture will, in most cases, work very similarly to the ones we have today – just like Coinbase works similarly to PayPal.

The big difference to consumers, however, is that because they are built on decentralized protocols, they will be able to talk to each other, just like different email applications and bitcoin wallets can interoperate.

One thing I like about this stack is that it’s growing from the bottom up. First we had miners, the blockchain, and bitcoin, and now we’re building everything else on top. As far as I know, the most significant revolutions in technology have been built this way." (http://www.coindesk.com/blockchain-application-stack/)

Why Blockchains don't scale

Preethi Kasireddy:

"Blockchains, as it stands today, are limited in their ability to scale.

That’s not to say that this will be the case forever, but it’s definitely true today. In fact, I’d argue it’s one of the biggest technological barriers we face with blockchain technology today. It’s quickly become a very active area of research among researchers in the community and cryptocurrency in general.

Why isn’t the blockchain scalable? Currently, all blockchain consensus protocols (eg. Bitcoin, Ethereum, Ripple, Tendermint) have a challenging limitation: every fully participating node in the network must process every transaction. Recall that blockchains have one inherent critical characteristic — “decentralization” — which means that every single node on the network processes every transaction and maintains a copy of the entire state.

While a decentralization consensus mechanism offers some critical benefits, such as fault tolerance, a strong guarantee of security, political neutrality, and authenticity, it comes at the cost of scalability. The number of transactions the blockchain can process can never exceed that of a single node that is participating in the network. In fact, the blockchain actually gets weaker as more nodes are added to its network because of the inter-node latency that logarithmically increases with every additional node.

In a traditional database system, the solution to scalability is to add more servers (i.e. compute power) to handle the added transactions. In the decentralized blockchain world where every node needs to process and validate every transaction, it would require us to add more compute to every node for the network to get faster. Having no control over every public node in the network leaves us in a pickle.

As a result, all public blockchain consensus protocols that operate in such a decentralized manner make the tradeoff between low transaction throughput and high degree of centralization. In other words, as the size of the blockchain grows, the requirements for storage, bandwidth, and compute power required by fully participating in the network increases. At some point, it becomes unwieldy enough that it’s only feasible for a few nodes to process a block — leading to the risk of centralization.

In order to scale, the blockchain protocol must figure out a mechanism to limit the number of participating nodes needed to validate each transaction, without losing the network’s trust that each transaction is valid. It might sound simple in words, but is technologically very difficult.

Why?

- Since every node is not allowed to validate every transaction, we somehow need nodes to have a statistical and economic means to ensure that other blocks (which they are not personally validating) are secure.

- There must be some way to guarantee data availability. In other words, even if a block looks valid from the perspective of a node not directly validating that block, making the data for that block unavailable leads to a situation where no other validator in the network can validate transactions or produce new blocks, and we end up stuck in the current state. (There are several reasons a node might go offline, including malicious attack and power loss.)

- Transactions need to be processed by different nodes in parallel in order to achieve scalability. However, transitioning state on the blockchain also has several non-parallelizable (serial) parts, so we’re faced with some restrictions on how we can transition state on the blockchain while balancing both parallelizability and utility."

(https://hackernoon.com/blockchains-dont-scale-not-today-at-least-but-there-s-hope-2cb43946551a)

(the above article discusses the technical solutions)

Business Models

Joel Dietz:

"There are currently a number of incentive structures surrounding blockchain technology and open source software:

(1) Contribute open source code and make money via services (i.e. Peter Todd’s consulting)

(2) Create a new close source software project based on the Bitcoin blockchain with a privately held speculative unit (i.e. legal equity in Coinbase)

(3) Create an new technology set plugged into the Bitcoin blockchain with a privately held speculative unit (i.e. legal equity in Blockstream/Sidechains)

(4) Create an entirely new unit with inherent utility on a new blockchain (BTC in Bitcoin, XRP in Ripple, ETH in Ethereum)

(5) Create an entirely new unit with inherent utility on the Bitcoin blockchain (MSC in Mastercoin, XCP in Counterparty)" (https://medium.com/@Swarm/the-second-wave-of-blockchain-innovation-270e6daff3f5)

The fundamental value proposition of the blockchain concerns verification and transaction costs

From an interview of Christian Catalini, by Paul Michelman of Sloan magazine:

"We started by asking ourselves: What fundamental costs does blockchain reduce? If you can answer this question, it becomes much easier to identify where the opportunities are, whether you are an established company, a startup, or a regulator. Applications that do not take advantage of the structural changes in costs that the technology allows for are unlikely to succeed, as they will have a difficult time convincing consumers and businesses to adopt. Similarly, solutions that claim benefits the technology cannot currently deliver are likely to fail. ... We concluded that at least two key costs will be affected: the cost of verifying the attributes of a transaction (for example, when did it take place, who was involved, etc.) and the cost of exchanging value within a network without relying on a costly intermediary.

The ability to securely record and time-stamp information on a blockchain is extremely valuable when issues arise with a transaction. Whereas today we often have to invest resources to audit the transaction and assess the truth, in the future, these tasks could be automated thanks to a distributed ledger. This makes settlement and reconciliation across organizations simpler and more efficient, which explains why many early use cases for blockchain are in the financial sector. Here the compelling reason to adopt is the ability to lower operational costs while keeping the rest of the ecosystem the same. It also explains why banks and financial institutions like distributed ledgers but are worried about cryptocurrencies. Distributed ledgers, on their own, do not challenge existing revenue models and regulatory frameworks. In fact, they may even allow incumbents to achieve greater economies of scale. Cryptocurrencies, in contrast, present an existential threat to how value is generated and appropriated in the economy.

This is where the second cost — the cost of networking — plays a key role: Before cryptocurrencies such as bitcoin existed, we needed intermediaries to transfer value across the globe. Creating and maintaining a secure network was both capital-intensive and labor-intensive. Bitcoin solves this problem by throwing cheap hardware at it: While often criticized for the energy-consuming computations needed to secure it, the bitcoin network has been extremely successful at automating value transfer. Where secure financial messaging platforms such as SWIFT and ACH have to invest in maintaining “trusted nodes” to validate transactions, Bitcoin uses a clever mix of cryptography and game theory to deliver the same results. Gone are the accounting, reconciliation, and security costs associated with ensuring that a rogue employee or financial institution did not tamper with the transaction. The integrity of the underlying data is not guaranteed by an intermediary but by the design of the system itself. This is the architectural innovation associated with cryptocurrencies, and it constitutes both an opportunity and a threat to existing business models."

Examples of the first ...

"Of course, the immutability offered by a distributed ledger is helpful only if the information it recorded is accurate in the first place. Hence, the cheaper it is to commit information early in the value chain and in an automated and tamperproof fashion, the better. Similarly, the more one can envision replacing labor-intensive and time-consuming tasks with a combination of software and a “shared source of truth,” the more the technology is likely to be useful. Early applications on this front range from the trading and settlement of currencies and financial assets to the tracking of ownership stakes in early-stage companies. For example, in 2015 Nasdaq experimented with executing a private securities transaction for San Francisco-based blockchain startup Chain Inc. on a distributed ledger, removing the manual steps typically involved in the process. Similarly, New York-based Digital Asset Holdings LLC is developing distributed ledger technology for the Australian Securities Exchange post-trade market, and startups such as Boston-based Circle Internet Financial Inc. and Plutus Financial Inc. (d/b/a Abra), based in Mountain View, California, are already using blockchain to lower the cost of transferring money across the globe."

Examples of the second:

"Changes in the cost of networking — although they will take longer to unfold — are more likely to be substantial. The ability to bootstrap a marketplace without the need for a central actor constitutes a radical departure from how most organizations appropriate value within their ecosystem today. Cryptocurrencies enable a hybrid type of organization that can take advantage of both the efficiency of a market and the more complex forms of contracting and governance that take place within companies or on online platforms. By sourcing capital, talent, and ideas through smart contracts, such organizations will be possibly able to move and allocate resources at a speed previously unimaginable. Many of the online platforms that rely today on their ability to process payments between buyers and sellers, and on controlling a reputation system (such as Uber Technologies Inc. and Airbnb Inc.) may face increased competition from open protocols that source resources and allocate returns in a more flexible way.

Early experiments in this space include startups like San Francisco-based Numerai LLC, a hedge fund that makes investment decisions on the basis of crowdsourced predictions generated by a distributed network of data scientists. The data scientists rely on a cryptocurrency to both disclose their confidence in their models and appropriate the returns from their contributions. In addition, a smart contract ensures that participants do not have an incentive to “overfit” their data, as rewards are linked to the long-run ability of the hedge fund to make good investment decisions." (https://sloanreview.mit.edu/article/seeing-beyond-the-blockchain-hype/)

Comparing the Incentive Models

Joel Dietz:

"For a long time, the primary model of open source software development has been in category one. The software itself is free. Hosting and other services around it are not. People can also build high value applications on top of the open source code, but these are usually closed source. This is the model that Ruby on Rails and other web frameworks have used fairly successfully as Joel Dietz has previously written.

The second model is the typical business model. In this, the structure of legal equity binds both investors and developers to a future value that may not be realized for several years. This typically creates a group of a few people who are highly committed to a particular outcome, but may naturally come into odds. Historically there is also no way to incentivize any of the parties beyond employees and investors that may also have a vested interest in the platform (i.e. power users).

The third model, by which I primarily refer to Sidechains, is still inchoate. In the Sidechains whitepaper it proposes demurrage as a method for incentivizing sidechain development. This seems to promote exactly the opposite set of incentives than what you would want. Effectively this means that assets on the main chain hold their value, while assets on a sidechain gradually decrease in value, while the difference is basically given away to miners. Also, the Sidechains project has no publicly stated business model, which is also a fairly significant concern. Any potential revenue on a service-based business will never be enough for the venture capitalists to get their necessary return, which basically forces them to either create a closed source product or otherwise leverage their position to “gate keep” and charge some sort of toll on network usage.

The fourth model, though strongly disliked by many, is ironically closest to Bitcoin itself. It states fundamentally that there can be a speculative unit with attached technological innovation that is acquired, and by which the speculators will benefit as both utility and network grows. The somewhat unique feature of Ethereum and a few other related projects (e.g. DarkCoin) is that unlike earlier “altcoins,” these new projects do have significant additional utility that is not found on the Bitcoin Blockchain.

Since all such projects extend the core Bitcoin technology with this additional utility, this effectively makes them competitors to the Bitcoin blockchain. Although early adopters and venture capitalist backers of Bitcoin had the hope that the network effects of Bitcoin would make it something like the TCP/IP protocal of internet money, it is entirely possible that some other competitor will surpass it. I suspect that whether or not this is the case will depend highly on whether or not anyone can make comparable utility and innovation compatible with Bitcoin.

This leads to a fifth model that was perhaps under-appreciated until Ethereum came along. This is the possibility that a metacoin, so called because it works via inserting metadata into Bitcoin transactions, could provide much of the increased utility provided via a smart contracting layer without creating its own blockchain.

Both four and five have very similar economic incentive structures. First of all, they are open to all participants and immediately liquid. Because of this it means that they naturally engage much more quickly a wider audience who are also incentivized to spread the word about that network. But, because of the immediate liquidity, there is no necessary long-term engagement. This affects both the development side and investing, and also means that there a fairly strong incentive to drive up the short time value for a project and exit at the peak. This likely results in a greater amount of capital, greater number of participants, with less depth. While potentially appropriate to the Facebook age, it is typically the case that startups require a few number of very intensely committed people due to the often intensely competitive nature of development, the occasional crisises that test resolve of key participants, and the general need for deferred compensation.

An additional problem is that none of these projects have evolved business models independent of the appreciation of their new asset class. All effectively depend on driving up the price by increasing the underlying utility of the unit and size of their related network, something that, while feasible, remains a questionable choice for anything that expects to be around in 5–10 years. Also, it is quite possible that price appreciation in such an asset is limited relative to the benefits traditionally associated with equity (i.e. 1000x returns on a successful software exit from an early investment). Since venture capital is generally structured as taking high rewards for high risk, projects with capped rewards impossible for them to undertake from an investment perspective.

Another very significant drawback is that even where economic incentives maybe aligned, there are basically no accountability structures due to the basically non-existant legal framework for entities receiving this sort of funding. In this case, Counterparty decided not to take funds whatsoever, whereas Ethereum structured their legal documentation to explicitly state that they were promising nothing in return whatsoever.

As Vitalik recently noted, Ethereum also has a problem of having a dual purpose “product” offering and an “investment” offering, something Swarm founder Joel Dietz called misaligned incentives in an early piece on economics of Ethereum. It is problems like these that have probably caused two out of three Counterparty founders to begin working for a private corporation (Overstock), presumably with some additional equity-based incentivization in addition to the base counterparty unit. In this case, the Counterparty ecosystem now has participants both in categories (4) and (2), with potential conflicts of interest between the participants in area (2), but also the possibility for larger ecosystem growth presuming that those conflicts can adequately be mediated.

So far we have only discussed the advantages and disadvantages of existing economic incentive structures. What about the future? What other possibilities can we expect to emerge?

The first “composite” offering has been proposed by Reddit. This is to take an existing equity offering and distribute the benefits downwards to community users via cryptocurrency. This is an incredible opportunity, because it illustrates one of the key benefits of this ‘open’ incentivization model, it actually directly compensates the community members who contribute to network growth.

The other model is Swarm itself, which, due to legal complexities, was deliberately vague about specific utility at the outset of its fundraising period, and instead described more generally the various categories of benefits that could be applied via these technologies (perk distribution, membership, privileged product access, financial rewards).

This was sometimes described as sort of crypto social-contract with the intention of providing as much value as possible to its users as the legal infrastructure was developed in order to do so. Much of this increased value depended on ability to structure agreements via smart contracts, which was a technology that did not even exist in any usable form until one week ago." (https://medium.com/@Swarm/the-second-wave-of-blockchain-innovation-270e6daff3f5)

Governance

On the difference between making rules and enforcing rules

By Izabella Kaminska:

"As Lehdonvirta observes, the vision of blockchain is of a system which can enforce contracts, prevent double spending, and cap the money supply pool without ceding power to anyone:

- No rent-seeking, no abuses of power, no politics — blockchain technologies can be used to create “math-based money” and “unstoppable” contracts that are enforced with the impartiality of a machine instead of the imperfect and capricious human bureaucracy of a state or a bank. This is why so many people are so excited about blockchain: its supposed ability change economic organization in a way that transforms dominant relationships of power. The problem which blockchain claims to have solved, in other words, is a rule-enforcement one, not a technological one.

And yet, here’s the rub. From Lehdonvirta:

- Unfortunately this turns out to be a naive understanding of blockchain, and the reality is inevitably less exciting. Let me explain why. In economic organization, we must distinguish between enforcing rules and making rules. Laws are rules enforced by state bureaucracy and made by a legislature. The SWIFT Protocol is a set of rules enforced by SWIFTNet (a centralized computational system) and made, ultimately, by SWIFT’s Board of Directors. The Bitcoin Protocol is a set of rules enforced by the Bitcoin Network (a distributed network of computers) made by — whom exactly? Who makes the rules matters at least as much as who enforces them. Blockchain technology may provide for completely impartial rule-enforcement, but that is of little comfort if the rules themselves are changed. This rule-making is what we refer to as governance.

Unfortunately for blockchain fanatics, there is no formal process for how governance works in bitcoin. Lehdonvirta says this is because for a long time the underlying politics were overlooked.

- … many people don’t recognize them, preferring instead the idea that Bitcoin is purely “math-based money” and that all the developers are doing is purely apolitical plumbing work. But what has started to make this position untenable and Bitcoin’s politics visible is the so-called “block size debate” — a big disagreement between factions of the Bitcoin community over the future direction of the rules.

Whatever model of the blockchain is employed, the fundamental problem of governance remains, says Lehdonvirta. What’s more, if it was somehow resolved… you’d no longer need a blockchain.

After all, as Lehdonvirta also observes, in performance terms, existing blockchain technologies are in many ways inferior to more conventional technologies." (https://ftalphaville.ft.com/2017/06/14/2190149/blockchains-governance-paradox/)

Potential Applications

by Dominic Frisby:

"Coders are now developing ways to use blockchain tech for purposes beyond an alternative money system. From 2017, you will start to see some of the early applications creeping into your electronic lives.

One application is in decentralised messaging. Just as you can send cash to somebody else with no intermediary using Bitcoin, so can you send messages – without Gmail, iMessage, WhatsApp, or whoever the provider is, having access to what’s being said. The same goes for social media. What you say will be between you and your friends or followers. Twitter or Facebook will have no access to it. The implications for privacy are enormous, raising a range of issues in the ongoing government surveillance discussion.

We’ll see decentralised storage and cloud computing as well, considerably reducing the risk of storing data with a single provider. A company called Trustonic is working on a new blockchain-based mobile phone operating system to compete with Android and Mac OS.

Just as the blockchain records where a bitcoin is at any given moment, and thus who owns it, so can blockchain be used to record the ownership of any asset and then to trade ownership of that asset. This has huge implications for the way stocks, bonds and futures, indeed all financial assets, are registered and traded. Registrars, stock markets, investment banks – disruption lies ahead for all of them. Their monopolies are all under threat from blockchain technology.

Land and property ownership can also be recorded and traded on a blockchain. Honduras, where ownership disputes over beachfront property are commonplace, is already developing ways to record its land registries on a blockchain. In the UK, as much as 50 per cent of land is still unregistered, according to the investigative reporter Kevin Cahill’s book Who Owns Britain? (2001). The ownership of vehicles, tickets, diamonds, gold – just about anything – can be recorded and traded using blockchain technology – even the contents of your music and film libraries (though copyright law may inhibit that). Blockchain tokens will be as good as any deed of ownership – and will be significantly cheaper to provide.

The Peruvian economist Hernando de Soto Polar has won many prizes for his work on ownership. His central thesis is that lack of clear property title is what has held back so many in the Third World for so long. Who owns what needs to be clear, recognised and protected – otherwise there will be no investment and development will be limited. But if ownership is clear, people can trade, exchange and prosper. The blockchain will, its keenest advocates hope, go some way to addressing that.

Smart contracts could disrupt the legal profession and make it affordable to all, just as the internet has done with music and publishing

Once ownership is clear, then contract rights and property rights follow. This brings us to the next wave of development in blockchain tech: automated contracts, or to use the jargon, ‘smart contracts’, a term coined by the US programmer Nick Szabo. We are moving beyond ownership into contracts that simultaneously represent ownership of a property and the conditions that come with that ownership. It is all very well knowing that a bond, say, is owned by a certain person, but that bond may come with certain conditions – it might generate interest, it might need to be repaid by a certain time, it might incur penalties, if certain criteria are not met. These conditions could be encoded in a blockchain and all the corresponding actions automated.

Whether it is the initial agreement, the arbitration of a dispute or its execution, every stage of a contract has, historically, been evaluated and acted on by people. A smart contract automates the rules, checks the conditions and then acts on them, minimising human involvement – and thus cost. Even complicated business arrangements can be coded and packaged as a smart contract for a fraction of the cost of drafting, disputing or executing a traditional contract.

One of the criticisms of the current legal system is that only the very rich or those on legal aid can afford it: everyone else is excluded. Smart contracts have the potential to disrupt the legal profession and make it affordable to all, just as the internet has done with both music and publishing.

This all has enormous implications for the way we do business. It is possible that blockchain tech will do the work of bankers, lawyers, administrators and registrars to a much higher standard for a fraction of the price.

As well as ownership, blockchain tech can prove authenticity. From notarisation – the authentication of documents – to certification, the applications are multifold. It is of particular use to manufacturers, particularly of designer goods and top-end electrical goods, where the value is the brand. We will know that this is a genuine Louis Vuitton bag, because it was recorded on the blockchain at the time of its manufacture.

Blockchain tech will also have a role to play in the authentication of you. At the moment, we use a system of usernames and passwords to prove identity online. It is clunky and vulnerable to fraud. We won’t be using that for much longer. One company is even looking at a blockchain tech system to replace current car- and home-locking systems. Once inside your home, blockchain tech will find use in the internet of things, linking your home network to the cloud and the electrical devices around your home.

From identity, it is a small step to reputation. Think of the importance of a TripAdvisor or eBay rating, or a positive Amazon review. Online reputation has become essential to a seller’s business model and has brought about a wholesale improvement in standards. Thanks to TripAdvisor, what was an ordinary hotel will now treat you like a king or queen in order to ensure you give it five stars. The service you get from an Uber driver is likely to be much better than that of an ordinary cabbie, because he or she wants a good rating.

There will be no suspect recounts in Florida! The blockchain will also usher in the possibility of more direct democracy

The feedback system has been fundamental to the success of the online black market, too. Bad sellers get bad ratings. Good sellers get good ones. Buyers go to the sellers with good ratings. The black market is no longer the rip-off shop without recourse it once was. The feedback system has made the role of trading standards authorities, consumer protection groups and other business regulators redundant. They look clunky, slow and out of date.